How Many Home Loans Can I Have

Ever found yourself staring at the ceiling, perhaps after a particularly inspiring episode of "Fixer Upper" or a dreamy scroll through Zillow, and wondered: "Can I actually pull off another mortgage?" It's a thought that tickles the fancy of many aspiring homeowners, or perhaps even seasoned property investors. The idea of multiple homes, each with its own unique charm and potential, is undeniably alluring. But before you start mentally redecorating your hypothetical beachfront villa and cozy mountain cabin, let's get down to the nitty-gritty: how many home loans can you actually have?

Think of it this way: your ability to get a mortgage isn't quite like collecting Pokémon. There's no definitive number that automatically caps you out. Instead, it’s more like a sophisticated balancing act, orchestrated by lenders who want to be sure you can juggle your financial commitments without dropping the ball. They're not just looking at your dreams; they're scrutinizing your reality.

The Lender's Crystal Ball: What They're Really Looking For

When you apply for a home loan, a lender essentially tries to predict your future financial behavior. It sounds a bit like fortune-telling, doesn't it? Except, instead of tarot cards, they use a combination of credit scores, debt-to-income ratios (DTI), and your overall financial stability. These are the key ingredients that determine how much risk they're willing to take on. And trust us, lenders are generally risk-averse, like a cat avoiding a bath.

Must Read

Your Credit Score: The VIP Pass

This is probably the most talked-about aspect of getting a loan, and for good reason. Your credit score is like your financial report card. A higher score signals to lenders that you're a responsible borrower who pays bills on time. Think of it as your golden ticket to more favorable loan terms and, crucially, the ability to qualify for multiple loans. If your score is consistently in the excellent range (think 740 and above), you're giving yourself a much wider playing field. It’s like having the best seats at a concert – you get access to the prime options.

On the flip side, a lower score might mean lenders are hesitant, or they might offer loans with higher interest rates. And while it’s technically possible to get multiple loans with a less-than-stellar score, it becomes exponentially harder and far less affordable. So, if your dream involves more than one mortgage, nurturing your credit score should be at the top of your to-do list. It’s the foundation upon which all your property aspirations are built.

Debt-to-Income Ratio (DTI): The Balancing Act

This is where things get a little more complex, but it’s absolutely vital to understand. Your DTI is a comparison of your monthly debt payments to your gross monthly income. Lenders use this to gauge your ability to manage monthly payments. Generally, they prefer your DTI to be around 43% or lower. This means that no more than 43% of your gross monthly income should go towards paying off all your debts, including your new mortgage(s), car payments, student loans, and credit card minimums.

So, if you already have one mortgage payment, that's already a significant chunk of your DTI. Adding another mortgage will increase that number. Lenders are looking at the total picture. Imagine you have a fantastic income, but also a mountain of other debts. Adding another mortgage could push your DTI into a zone that makes lenders nervous. It's less about the number of loans and more about the burden they represent relative to your income. Think of it as a scale: you want to keep it balanced with your income on one side and your debts on the other.

Different Loan Types, Different Rules

Now, here's where it gets interesting. Not all home loans are created equal, and the type of loan you get can influence how many you can have. Let's break down a few common scenarios:

Primary Residence vs. Investment Property

This is a big one. Loans for your primary residence (the home you live in) often come with more favorable terms and lower interest rates. Lenders see this as less risky because you're invested in maintaining your living space.

Loans for investment properties (where you plan to rent out or flip) are a different ballgame. Lenders often require larger down payments and might have slightly higher interest rates. They view these as more speculative. So, while you might be able to get a mortgage for your primary home and then another for a vacation rental, the qualifications for that second loan will be different.

It’s important to be upfront with your lender about the purpose of the property. Trying to sneak a vacation home past them as a primary residence is a big no-no and can have serious consequences.

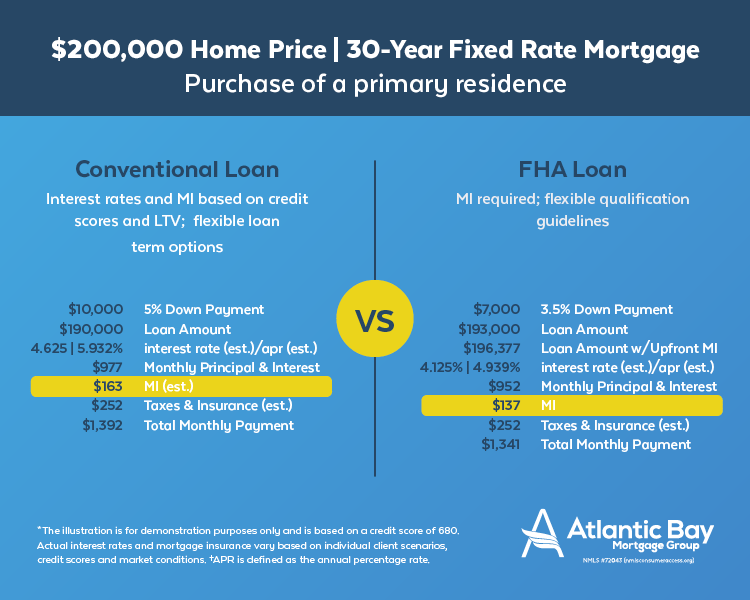

Conventional vs. Government-Backed Loans

Conventional loans are those not backed by a government agency. They typically follow the guidelines set by Fannie Mae and Freddie Mac. These are the workhorses of the mortgage world and are often what people use for multiple properties, provided they meet the strict DTI and credit score requirements.

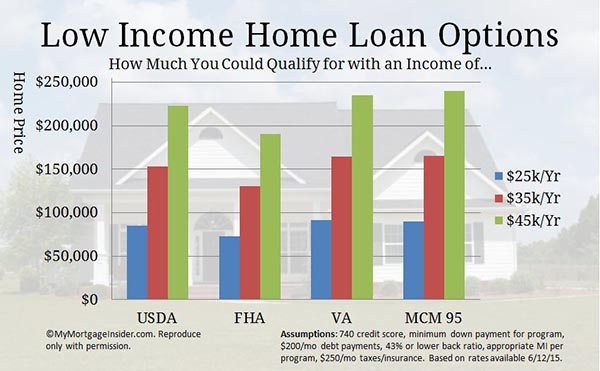

Government-backed loans, like FHA (Federal Housing Administration) and VA (Department of Veterans Affairs) loans, are designed to help specific groups of people, such as first-time homebuyers or veterans. These often have more lenient qualification requirements, but there's usually a catch: you can typically only have one FHA or VA loan at a time as your primary residence.

Once you move out of an FHA or VA-financed home and make it a rental, you might be able to qualify for another FHA or VA loan on a new primary residence. However, this can get complicated, and lenders have specific rules for this. It's always best to consult with a mortgage professional to navigate these nuances. Think of these government loans as special-use tools – great for their intended purpose, but not designed for a broad portfolio.

Jumbo Loans

If you're eyeing a property that's significantly more expensive than the conforming loan limits set by Fannie Mae and Freddie Mac, you'll be looking at jumbo loans. These come with their own set of stringent requirements, often demanding higher credit scores, larger down payments, and more significant reserves of cash. Juggling multiple jumbo loans would require a truly exceptional financial profile. It's like playing chess at the grandmaster level – the stakes are higher, and the strategy needs to be impeccable.

The Practicalities: What You Really Need to Consider

Beyond the lender's checklist, there are other practical aspects to ponder when thinking about multiple home loans. It's not just about getting approved; it's about sustainable ownership. This is where the lifestyle aspect really kicks in.

Your Financial Foundation: Beyond the Minimums

Lenders look at your ability to make monthly payments, but they also want to see that you have a cushion. This means having significant savings or liquid assets. They want to know that if your tenant skips town for a month, or if you have an unexpected repair bill on one of your properties, you won't be scrambling to make your mortgage payments. This is often referred to as having adequate "reserves."

A good rule of thumb is to have enough reserves to cover several months of mortgage payments (principal, interest, taxes, and insurance – PITI) on all your properties. This shows a level of financial maturity and preparedness that lenders appreciate. It’s like having a spare tire in your car – you hope you never need it, but you’re incredibly glad it’s there when you do.

![How Many Home Loans Can One Person Have? - Complete Guide [2024]](https://www.aavas.in/uploads/images/blog/how-many-home-loans-can-one-person-have-1890664358.jpg)

The Ghost of Future Interest Rates

Interest rates are a huge factor. When you have multiple mortgages, especially if they’re at different times, you’re subject to the prevailing interest rates at the time of each application. If rates are high when you apply for your second or third loan, your monthly payments will be significantly higher. This can impact your DTI and your overall affordability. Timing is everything, as they say, and in the mortgage world, it’s especially true.

Think about the economic climate. Are interest rates on the rise? Are they at historic lows? Understanding these trends can help you strategize when to pursue another mortgage. It’s like predicting the weather – you wouldn’t plan a picnic in a hurricane, and you probably shouldn’t embark on a mortgage spree during a period of rapidly increasing interest rates.

The Joy (and Stress) of Management

Let's not forget the human element! Owning one home is a commitment. Owning multiple homes? That's a whole new level of dedication. You'll be dealing with maintenance, repairs, property taxes, insurance, and potentially managing tenants. If these are investment properties, this can become a full-time job in itself. Are you prepared for the time commitment and the potential headaches?

This is where the lifestyle choice comes into play. Do you envision yourself as a laid-back landlord, or are you someone who thrives on the hustle? If you're aiming for a relaxed, stress-free lifestyle, perhaps one well-managed property is more your speed than a sprawling portfolio. Think of it like choosing between a single, perfect succulent or an entire jungle to tend to.

So, How Many is "Too Many"?

There isn't a magic number dictated by law or a universal lender policy that says "Thou shalt have no more than X home loans." The answer is deeply personal and hinges on your individual financial circumstances. However, common wisdom and lender practices suggest:

- For most individuals aiming for a comfortable lifestyle with minimal financial strain, one or two mortgages are generally manageable. This allows for a primary residence and perhaps a vacation home or a modest investment property without overly stretching your finances.

- Three or more mortgages often indicate a serious investor profile, requiring a robust income, excellent credit, significant down payments, substantial reserves, and a clear strategy for managing multiple properties. This is where the risk profile for lenders increases significantly.

Ultimately, the number of home loans you can have is limited by your capacity to qualify and your ability to comfortably service the debt. Lenders are the gatekeepers, and your financial health is the key that unlocks their doors. It's less about a hard limit and more about a sustainable financial reality.

Think about it this way: if you have a stellar credit score, a DTI that looks like a well-tuned engine, and a healthy savings account, you might be able to swing more than the average person. But even then, it's crucial to be realistic about what you can handle financially and emotionally. A portfolio of homes is exciting, but a mountain of debt is not. It’s about finding that sweet spot where your dreams align with your financial well-being.

A Little Fun Fact

Did you know that in the US, the average number of homes owned per person isn't a readily tracked statistic? However, surveys show that a significant portion of wealth is tied up in real estate. This suggests that while many people aspire to homeownership, owning multiple properties is still a more exclusive club. It's like a Michelin-starred restaurant – coveted, but not for everyone's daily dining.

The Takeaway: It's Your Financial Symphony

The pursuit of multiple homes is a grand ambition, and it’s absolutely achievable for some. But it’s a journey that requires careful planning, financial discipline, and a realistic understanding of what lenders are looking for. It’s not just about acquiring property; it’s about building a stable and enjoyable financial future.

So, as you gaze at those inspiring online listings or daydream about your next real estate venture, remember that the number of home loans you can have is less a fixed number and more a reflection of your financial symphony. Are the instruments playing in harmony, or is it a cacophony of debt? The goal is to conduct a beautiful, sustainable melody of homeownership that brings you joy, security, and perhaps a little extra rental income.

In the end, whether you have one mortgage or several, the most important thing is that it serves your lifestyle and brings you peace of mind. A home, after all, is meant to be a sanctuary, not a source of constant stress. So, take a deep breath, crunch those numbers, and dream big – but dream smart!