Is It A Good Idea To Remortgage

Sarah was staring at her bank statement, a familiar knot of anxiety tightening in her stomach. It was that time of year again – the annual check-in with her mortgage lender. For the past five years, her payments had been a steady, predictable chunk of her income. But lately, she’d been hearing whispers from friends, seen a few too many targeted ads, and even her mum had casually mentioned, "Have you thought about remortgaging, dear? Rates are looking quite appealing." It felt like everyone was doing it, and Sarah, bless her heart, was always a little behind the curve. She imagined herself at a secret mortgage party, everyone else in the know, while she was still fumbling with her old, slightly embarrassing 90s calculator.

This feeling of being on the outside of a potentially good deal is what prompted this whole deep dive. Because let's be honest, the word "remortgage" can sound a bit… serious. Like filing taxes, or attending a mandatory corporate team-building event. But what if it’s actually not that scary? What if it’s more like discovering a shortcut on your commute, or finding out your favourite café has a secret menu? That’s what we’re here to explore.

Remortgaging: Is It Your Next Big Money Move?

So, you’ve got a mortgage. Congratulations, you’re a homeowner! (Or maybe you're just paying off a very large loan, but let's stay positive, shall we?) Now, the question looms: is it a good idea to remortgage? It’s not a simple yes or no, like deciding whether to have a second biscuit. It’s a bit more nuanced, a bit more like choosing the right biscuit for your tea.

Must Read

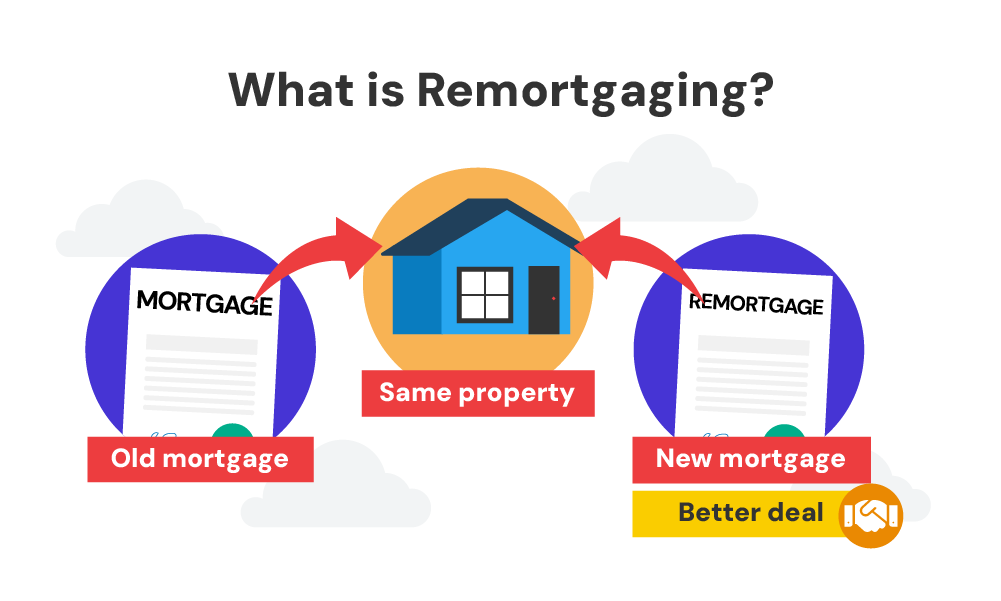

Essentially, remortgaging means taking out a new mortgage on your property to replace your existing one. Think of it as ditching your old phone for the latest model, but for your house. You're usually looking for better terms, a different interest rate, or maybe even to borrow a bit more cash. Simple enough, right? Except, like anything involving the word "mortgage," there are details.

Why Would Anyone Bother Remortgaging? The Big Questions.

Let’s get down to the nitty-gritty. What’s in it for you? Why would you go through the hassle of changing your mortgage? The main drivers usually boil down to a few key things:

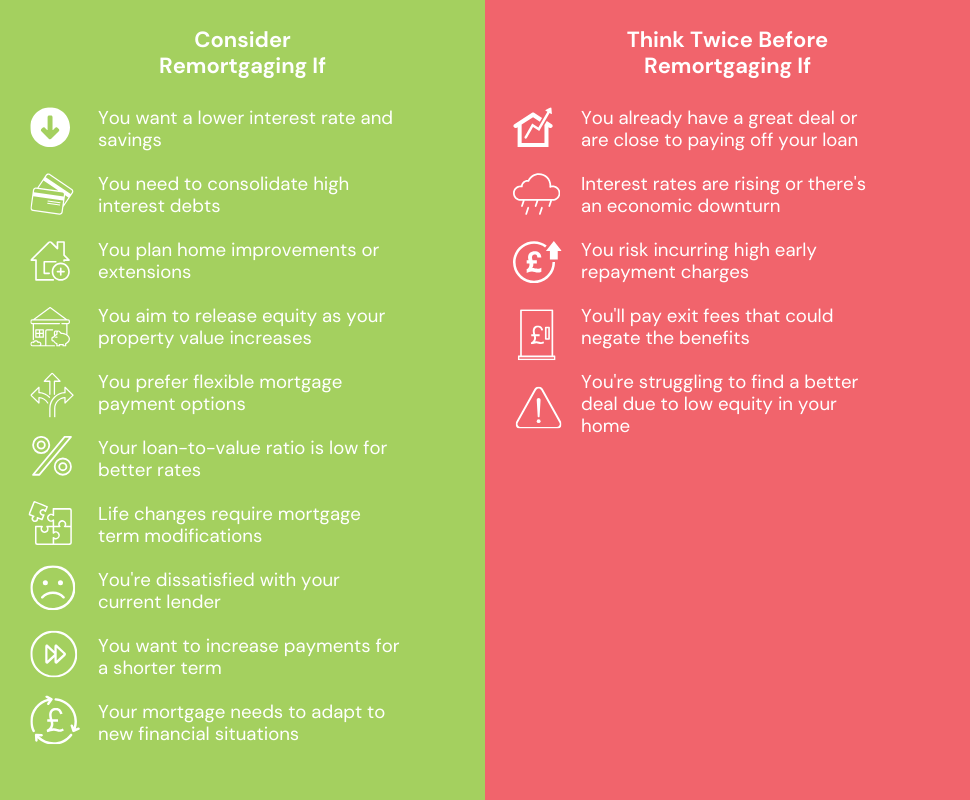

Saving Money on Interest: This is the big kahuna, the main event. If interest rates have dropped significantly since you first got your mortgage, or if your current lender’s introductory rate is about to expire and you’ll be moved onto a higher standard variable rate, then remortgaging to a lower rate could save you a substantial amount of money over the life of your loan. Imagine finding a £20 note in an old coat pocket, but consistently, every month. That’s the dream!

Cutting Your Monthly Payments: Even if the overall interest saved isn’t astronomical, a lower interest rate can mean lower monthly repayments. This can free up a surprising amount of cash in your budget. Suddenly, that holiday you’ve been eyeing, or the emergency fund you’ve been meaning to build, feels a lot more attainable. It’s like your mortgage is suddenly sighing with relief, and so are you.

Switching Lenders: Sometimes, your current lender might not be the most competitive anymore. There are so many lenders out there, all vying for your business. By remortgaging, you can often move to a lender offering better deals, more flexible terms, or a more user-friendly online experience (because let's face it, some online portals feel like they were designed in the dial-up era).

Borrowing More Money: Need to fund a home renovation? Pay for your kids’ university fees? Consolidate some high-interest debt? Remortgaging can allow you to borrow additional funds against the equity you’ve built up in your home. This is often called a "remortgage with a top-up" or "further advance." It’s a way to leverage your property’s value, but it definitely requires careful consideration. Think of it as tapping into your house’s piggy bank. Just make sure you’ve got a clear plan for what you’re going to spend it on!

Moving to a Fixed Rate: If you’re currently on a variable rate and are worried about interest rates rising, remortgaging to a fixed-rate mortgage can provide certainty. You’ll know exactly what your repayments will be for the duration of the fixed term, offering peace of mind in an unpredictable economic climate. No more sleepless nights wondering if your direct debit is about to go up by £100.

Okay, But What's the Catch? (There's Always a Catch, Right?)

Ah, the eternal question. Nothing in life is truly free, and remortgaging isn't an exception. There are costs involved, and you need to weigh them up against the potential savings. This is where Sarah’s calculator might come out after all.

Fees, Fees Everywhere! You’ll likely encounter various fees when you remortgage. These can include:

- Arrangement fees: A fee charged by the new lender to set up the mortgage. This can be a fixed amount or a percentage of the loan.

- Valuation fees: The lender needs to assess the value of your property.

- Legal fees: You’ll need a solicitor or conveyancer to handle the legal paperwork.

- Early Repayment Charges (ERCs): This is a crucial one! If you’re currently in a fixed-rate or introductory period with your existing mortgage, you might have to pay a penalty to switch before that period ends. This can sometimes negate all the potential savings, so always check your current mortgage contract very, very carefully. It’s like trying to leave a party early and the host charges you a "leaving fee."

Impact on Your Credit Score: The remortgaging process involves a credit check. While a single check is unlikely to have a major impact, applying for multiple mortgages in a short space of time can potentially lower your score. So, be strategic and do your research beforehand.

The Application Process Itself: It’s not just a quick form fill. You’ll need to gather lots of documentation (payslips, bank statements, proof of identity, etc.) and go through an application and underwriting process. It can take time and effort, and sometimes feels like a job interview for your own house.

When Does Remortgaging Make Sense? The Magic Formula.

So, when is it a no-brainer? Or at least, a strong consideration?

When your current fixed-rate or introductory deal is ending: This is probably the most common and often the most beneficial time. If you’re about to be rolled onto a Standard Variable Rate (SVR) which is usually higher than competitive fixed rates, looking for a new deal is almost always a good idea. Don’t just stick with your current provider out of inertia – they’re counting on it!

When interest rates have fallen significantly: If the general mortgage market rates have dropped since you last secured your mortgage, you could benefit from a lower interest rate, even if you’re not at the end of a deal. You’ll need to calculate if the potential interest savings outweigh any early repayment charges.

When you need to borrow more money: If your circumstances have changed and you need a lump sum for a significant expense, remortgaging to release equity can be an option. Just be realistic about your ability to repay the increased borrowing.

When you want to switch from a variable to a fixed rate for stability: If the thought of fluctuating monthly payments gives you hives, moving to a fixed rate can offer welcome predictability. This is especially true in uncertain economic times.

How Do I Even Start? Your Action Plan.

Feeling a bit less daunted? Good. Here’s a roadmap to navigating the remortgaging maze:

1. Figure Out Your Current Mortgage Details.

Dig out your mortgage statement. Know your outstanding balance, your current interest rate, the type of rate you’re on (fixed, variable, SVR?), and crucially, if there are any early repayment charges and when your current deal ends. This is your baseline.

2. Assess Your Financial Situation.

Be honest with yourself. What’s your income? What are your outgoings? Can you comfortably afford the current payments? Can you afford potentially higher payments if you borrow more? Your credit score will also be a factor, so it’s worth checking it beforehand.

3. Work Out the Potential Savings.

This is where the maths comes in. Use online mortgage calculators (they’re much better than Sarah’s old calculator!) to compare your current deal with potential new offers. Factor in all the fees associated with remortgaging. Don’t just look at the headline interest rate; look at the Annual Percentage Rate of Charge (APRC), which includes most of the fees and gives a more accurate picture of the overall cost.

4. Explore Your Options.

This is where you can either do it yourself or get professional help.

- Directly with Lenders: You can research and apply directly to lenders. This gives you direct control but requires more legwork.

- Mortgage Brokers: A mortgage broker works for you, not a specific lender. They can access deals from a wide range of lenders, including some that aren’t available on the high street. They can also help with the application process and advise you on the best products for your situation. Their advice can be invaluable, and they’ll often have access to deals you wouldn’t find yourself.

5. Gather Your Documents.

Be prepared to provide proof of income (payslips, P60), bank statements, proof of identity, and details of your current mortgage. The more organised you are, the smoother the process will be.

6. Compare, Compare, Compare!

Don’t settle for the first offer you see. Look at the interest rate, the fees, the loan term, any incentives (like cashback), and the lender’s reputation for customer service. The cheapest headline rate isn’t always the best overall deal.

7. The Application and Approval Process.

Once you’ve chosen a mortgage, you’ll submit your application. The lender will carry out a valuation of your property and your credit checks. If all goes well, you’ll receive an offer. Your solicitor will then handle the legal transfer of the mortgage.

The Bottom Line: Is It Worth It For Sarah?

So, back to Sarah. She’s not at a secret mortgage party. She’s just a regular person, navigating the complexities of homeownership. Remortgaging isn’t some mystical ritual reserved for the financially savvy. It’s a tool. A tool that, when used wisely, can help you save money, gain financial flexibility, and secure your future. But like any tool, it needs to be used correctly and at the right time.

The key is to do your homework. Understand your current situation, research your options thoroughly, and crunch the numbers. Don’t be afraid to ask questions, and consider seeking advice from a qualified mortgage advisor. They’ve seen it all before and can guide you through the jargon and the fine print.

For Sarah, and for you, the decision to remortgage hinges on whether the potential benefits – like lower monthly payments or significant interest savings – outweigh the costs and the effort involved. It might be the smartest financial move you make this year, or it might be a lot of fuss for very little gain. But you won’t know unless you investigate, will you?

So, maybe Sarah should fire up her laptop, dust off her financial documents, and see what’s out there. It might be the start of a much more comfortable financial journey. Or at the very least, she’ll have a much better understanding of what everyone else has been gossiping about. And that, in itself, is a win.