Usaa Cd Early Withdrawal Penalty

Hey there! So, you're probably wondering about this whole "USAA CD early withdrawal penalty" thing, right? Maybe you've got a Certificate of Deposit with them and life just threw you a curveball. Or, maybe you're just doing your homework before committing your hard-earned cash. Whatever the reason, you've landed here, and I'm happy to chat about it. Think of me as your friendly, slightly caffeinated guide through the slightly less-than-thrilling world of early CD withdrawals.

First off, let's get one thing straight: CDs are awesome for saving money. They're like a piggy bank that promises not to let you spend its contents until a certain date. This promise is what gives them their good interest rates. But, like any promise, breaking it early usually comes with a little… well, let's call it a "thank you" gift to the bank for holding your money for you. And that gift is the early withdrawal penalty. No sugarcoating it!

Now, USAA is known for being pretty darn good to its members. They’re military-focused and generally have a solid reputation. So, when it comes to their CDs, you can expect them to be upfront about the rules. And the biggest rule with a CD, the one that makes you want to slap a sticky note on it saying "DO NOT TOUCH UNTIL [MATURITY DATE]", is that early withdrawal will cost you.

Must Read

So, what exactly is this penalty? It’s not like they’re going to send a squad of tiny, money-collecting robots to your house. Phew! For USAA CDs, the penalty is typically calculated based on a certain amount of the interest you've already earned. Think of it like this: the bank gave you a little bonus (interest) for keeping your money with them. If you decide to dip out before the agreed-upon time, they take back a portion of that bonus as a fee. It's their way of saying, "Hey, we appreciate you keeping your word, and if you can't, that's okay, but here's a little something for your trouble."

USAA's Specific Penalty Policies: The Nitty-Gritty (but not too gritty!)

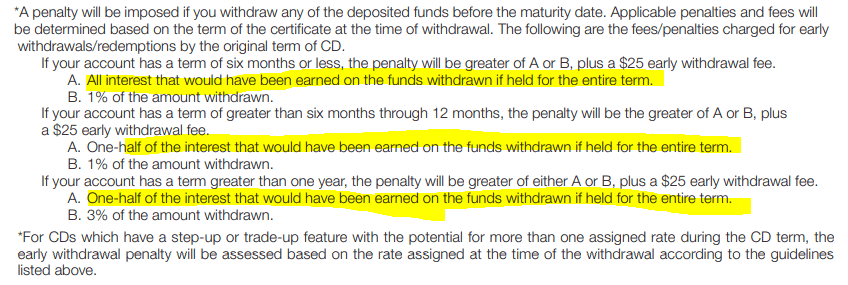

Alright, let's get a little more specific, because that's what you came here for, right? While the exact penalty can sometimes vary slightly depending on the specific CD term you chose (like a 1-year CD versus a 5-year CD), USAA generally follows a pretty standard structure. For most of their CDs, the penalty is often equivalent to a certain number of months' worth of interest. For example, it might be 90 days' interest for shorter-term CDs, or 180 days' interest for longer-term ones.

This means if you’ve only had your CD for a short period, and haven’t earned much interest yet, the penalty could eat up all the interest you've made, and then some. That’s the part that can feel a bit like a gut punch. Imagine opening your piggy bank and finding out the candy you bought with your allowance cost you double because you ate it before dinner. Ouch!

Why does this penalty exist? It’s all about supply and demand, my friend. Banks offer you a good interest rate because they know they can rely on having your money for a fixed period. They use that money to fund loans and other financial activities. If everyone suddenly decided to pull their money out early, it would mess up their whole system. So, the penalty is there to encourage people to stick to their savings plan and to compensate the bank for any inconvenience or potential loss they might incur if you break the agreement.

So, what happens if you absolutely have to withdraw early? Let's say, hypothetically, your beloved pet iguana suddenly needs a solid gold diamond-encrusted water dish (hey, no judgment!). You'd look at the penalty, right? You'd calculate how much interest you've earned and then subtract the penalty. If your penalty is more than the interest you've earned, then you're dipping into your principal. That's the big no-no. You want to avoid touching that original chunk of money if at all possible.

Here’s a little trick to help you figure it out: when you open your USAA CD, you should have received a CD disclosure document. This document is your treasure map to all things CD-related, including the penalty for early withdrawal. Keep it somewhere safe, or if you're tech-savvy, save it digitally. It's usually the most accurate place to find the specific terms for your CD.

Decoding the Disclosure: Your Secret Weapon

This disclosure document is your best friend when it comes to understanding these penalties. It will clearly state things like:

- The APY (Annual Percentage Yield) of your CD.

- The term of your CD (how long it's locked up).

- The exact penalty for early withdrawal. This is crucial! It might say something like "a forfeiture of 180 days of interest" or "a penalty of X% of the withdrawal amount."

Let’s do a quick, super-simplified example. Let’s say you have a $10,000 CD with USAA, and the penalty is 90 days of simple interest. And you’ve had it for 6 months. If the interest rate is, say, 4% APY, you can do some quick math (or a quick online calculator!) to figure out roughly how much interest you’ve earned. Then, you’d calculate 90 days of interest at that rate. If that 90 days of interest is less than the total interest you've earned in 6 months, you're probably in the clear to withdraw without losing any principal. But if it's more, or if you haven't earned enough interest to cover it, you'll be losing some of your original investment. See why that disclosure is important?

It's also worth noting that some very short-term CDs (like 30 or 60 days) might have a different penalty structure, or sometimes even no penalty for early withdrawal, though these are less common. USAA's website and your CD disclosure will be your definitive guides here.

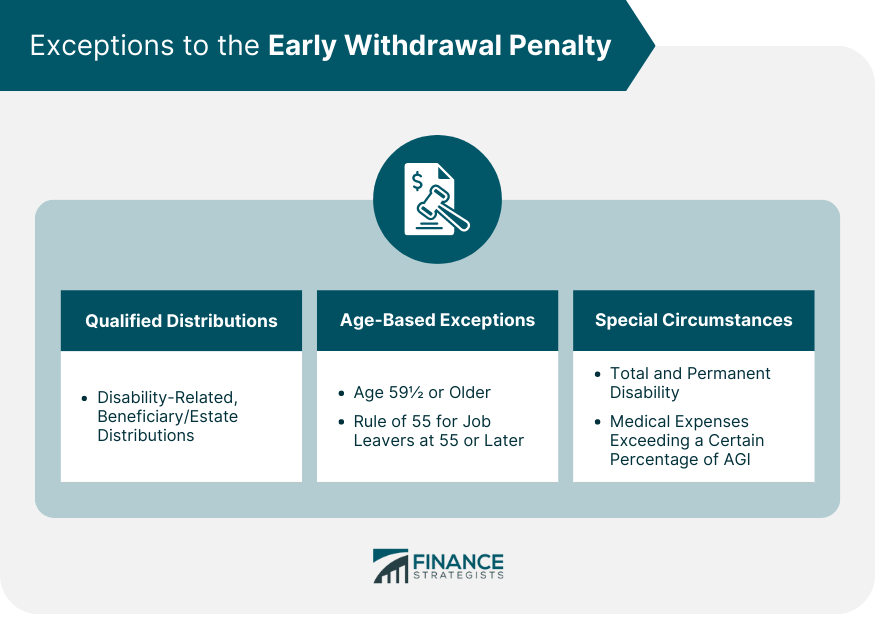

What if it’s an emergency? Life happens, and sometimes emergencies trump even the best-laid savings plans. USAA, being a member-focused institution, might have some flexibility in extreme circumstances. It never hurts to call their customer service line and explain your situation. They can't promise anything, but a friendly chat might reveal some options you didn't know existed. They're not monsters, after all!

Avoiding the Pitfalls: Smart Strategies

So, how can you avoid the dreaded early withdrawal penalty altogether? It’s all about planning and being realistic with your savings goals.

- Match the CD term to your goals: If you know you'll need the money within a year, don't lock it up in a 5-year CD. This is like trying to fit a square peg in a round hole – it’s just not going to end well.

- Build an emergency fund: This is your first line of defense! Before you even think about CDs, make sure you have a readily accessible savings account with enough money to cover 3-6 months of living expenses. This way, unexpected costs don't force you to raid your long-term savings.

- Diversify your savings: Don't put all your eggs in one basket. Keep some money in a regular savings account for immediate needs, and then use CDs for money you're confident you won't need for a while.

- Look for "no-penalty" CDs: Some institutions offer CDs that allow you to withdraw your money penalty-free after a certain grace period (usually around 7 days after opening or a specific number of days after maturity). USAA might offer these from time to time, so keep an eye out!

- Read the fine print (I know, I know, but seriously!): Before you sign anything, make sure you understand the terms and conditions. It’s a small investment of your time that can save you a lot of headaches (and money!) down the line.

What about interest earned after the penalty? This is a common question. Let's say the penalty is 180 days of interest, and you withdraw after 200 days. You've earned interest for those 200 days. The penalty will then be deducted from that earned interest. If the penalty is less than the interest earned, you get the remaining interest. If it's more, and you haven't touched your principal, you’re still okay on that front. The key is to avoid touching your original deposit!

It can sound a little intimidating, can't it? But really, it’s just a way for banks to manage their money and for you to commit to a savings goal. Think of it as a gentle nudge from your future self to stay on track.

USAA's customer service is your friend! Seriously, if you're ever unsure about anything, pick up the phone or use their online chat. They're usually super helpful and can clarify any confusion about your specific CD and its penalty. They're the experts, and they're there to help you navigate these things.

So, while the USAA CD early withdrawal penalty is a real thing, it’s not some insurmountable obstacle. It’s a consequence of breaking an agreement, and like most consequences, it's there to encourage thoughtful decision-making. By understanding the rules, planning your savings goals wisely, and keeping your important documents handy, you can navigate the world of CDs with confidence and keep your financial journey smooth sailing.

And hey, even if you do have to withdraw early and incur a penalty, remember that life is about learning and adapting. That $100 penalty might sting a bit, but it’s likely a small blip in your overall financial journey. The fact that you're saving and thinking about your money is fantastic! Keep up the great work, stay informed, and remember that every step you take towards financial security is a victory. You've got this!