Interest Only Mortgage

Alright, buckle up, my home-buying adventurers! Let's chat about something that sounds a little bit… well, fancy. But trust me, it’s actually designed to make your wallet do a little happy dance. We’re talking about the Interest-Only Mortgage. Sounds like a secret handshake for millionaires, right? Nope! It’s more like a clever little trick that can give you some breathing room when you first snag your dream pad.

Imagine this: You’ve finally found "the one" – that cozy bungalow, that sprawling family home, that quirky loft with the killer city views. You’re practically floating on a cloud of freshly painted walls and the smell of new beginnings. But then, the numbers. Oh, the numbers! Mortgages can sometimes feel like a giant puzzle where all the pieces are trying to escape. And the monthly payment? Sometimes it feels like it’s trying to make a break for it too, dragging your budget along for the ride.

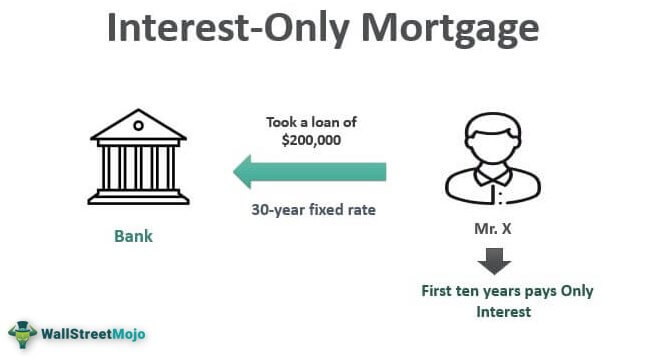

This is where our superhero, the Interest-Only Mortgage, swoops in. Think of it like this: When you buy a house, you’re essentially borrowing a huge chunk of cash from a friendly bank (or a less-friendly one, depending on your negotiation skills!). Normally, your monthly payment is a two-part punch: one part pays off the actual money you borrowed (the principal), and the other part pays the bank for the privilege of borrowing their money (the interest). It’s like renting a really, really expensive tool – you pay to use it, and eventually, you’d hope to own it.

Must Read

But with an Interest-Only Mortgage, for a set period of time (think of it as a super-fun introductory offer, maybe 5, 7, or 10 years!), your monthly payment is just the interest. That’s right! You’re not chipping away at the actual cost of your house during this initial phase. It’s like saying, “Hey bank, thanks for the loan! For a while, I’ll just pay you for letting me use your cash. The actual house? We’ll get to that later, when I’ve got my sea legs.”

So, what’s the big deal? Why would anyone not pay down their principal? Well, for starters, it means your monthly payments are significantly lower during that interest-only period. Imagine the possibilities! Maybe you want to do a spectacular kitchen renovation that’ll make your neighbors green with envy. Maybe you’ve got a dream vacation to Bora Bora that’s been simmering on the back burner. Or perhaps you just want to build up a healthier emergency fund because, let's face it, life throws curveballs, and it’s nice to have a cushion that doesn’t feel like a deflated pool toy.

It’s like getting a temporary superpower. Suddenly, your budget has a little more wiggle room. That’s the magic! You can funnel that extra cash into other things you care about, like investing in your future, starting that side hustle you’ve been dreaming about, or simply enjoying life a little more without feeling like every single penny is accounted for. It’s giving your wallet a well-deserved spa day!

Think of it like this: You’re building a magnificent sandcastle on the beach. The whole castle is your house. The principal is the sand you’re piling up to make the walls strong. The interest is the gentle lapping of the waves that come and go. With an Interest-Only Mortgage, for a while, you’re letting the waves just wash over the shore. You’re not actively adding more sand to the walls yet, but you’re enjoying the prime beachfront property! You’re getting settled, decorating your castle, and maybe even hiring some tiny crab architects to help with the moat.

And here’s the really exciting part: when that interest-only period ends (and it’s always a set period, so you know when the change is coming, no nasty surprises!), your payments will go up because you’ll then be paying both principal and interest. But by then, you’ll have had some serious time to save, invest, or pay down other debts. You'll be in a much stronger financial position to handle those slightly larger payments. It’s like a strategic head start!

It’s particularly appealing for folks who expect their income to rise significantly in the near future. Maybe you’re just starting your dream career, and you know a huge promotion is on the horizon. Or perhaps you’re expecting an inheritance. An Interest-Only Mortgage can be a fantastic tool to get into your home now and let your future earnings do the heavy lifting later. It’s like getting a head start on the race, knowing you’ve got the stamina to finish strong.

Now, of course, like any financial decision, it's not a one-size-fits-all magic wand. It’s super important to chat with a knowledgeable mortgage professional, someone who speaks fluent "finance" but can also explain it in plain English. They’ll help you understand if this is the right move for your unique situation. They’re like your financial sherpas, guiding you up the mountain of homeownership.

But if you’re looking for a way to ease into homeownership, to give yourself some immediate financial breathing room, and to potentially free up cash for other important goals, the Interest-Only Mortgage is definitely worth a closer look. It’s a clever way to make that dream home a reality, with a little extra sunshine for your budget along the way. So go ahead, dream big, and let your homeownership journey be as fun and manageable as possible!