How To Dissolve A Company In Uk

So, you've got a business in the UK, and for whatever reason, it's time to say goodbye. Maybe it's been a wild ride and it's time for a new adventure, or perhaps it's just served its purpose. Whatever the story, shutting down a company isn't quite as dramatic as a movie finale, but it does have its own set of steps. Think of it like carefully packing up a beloved, but no longer used, set of toys. You want to make sure everything's accounted for and put away properly, right? It’s actually pretty fascinating how the UK has a structured way of doing this, ensuring everything is tidy and legal.

Let's dive into the world of "dissolving a company in the UK." Sounds a bit formal, doesn't it? But honestly, it's just about officially ending your company's life. It's like when a character in a book has their arc completed, and the author closes their chapter. Pretty neat, when you think about it!

So, Why Would You Even Want To Close Up Shop?

You might be wondering, "Why would anyone willingly shut down a perfectly good company?" Well, life happens! Maybe your brilliant idea has run its course, and you're ready to brainstorm something even more exciting. Or perhaps the market shifted, and your business just isn't the right fit anymore. It could be that you've achieved your goals and it's time to hang up your business hat. Sometimes, it’s simply about simplifying things. Imagine having a cupboard full of gadgets you never use; eventually, you might just decide to clear it out. That's kind of what dissolving a company is like – a good declutter for your business life!

Must Read

Another reason could be if the company simply isn't trading anymore and you don't want the administrative hassle of keeping it on the books. Think of it as getting rid of a subscription you no longer use. It saves you time and, importantly, prevents any unnecessary fees or penalties down the line. It’s a responsible step, really.

The Two Main Paths to Company Closure

Now, when it comes to saying "ta-ta" to your company, there are generally two main routes you can take. It's like choosing between a gentle coasting out and a more deliberate, planned departure.

1. Striking Off (The "Easy-Peasy" Way, Sometimes!)

This is often the simplest and quickest route, especially if your company hasn't been active for a while and you owe no money. Think of striking off as if your company is like a ship that’s sailed its last voyage and is now peacefully docking. You're essentially asking the government to remove your company from the official register.

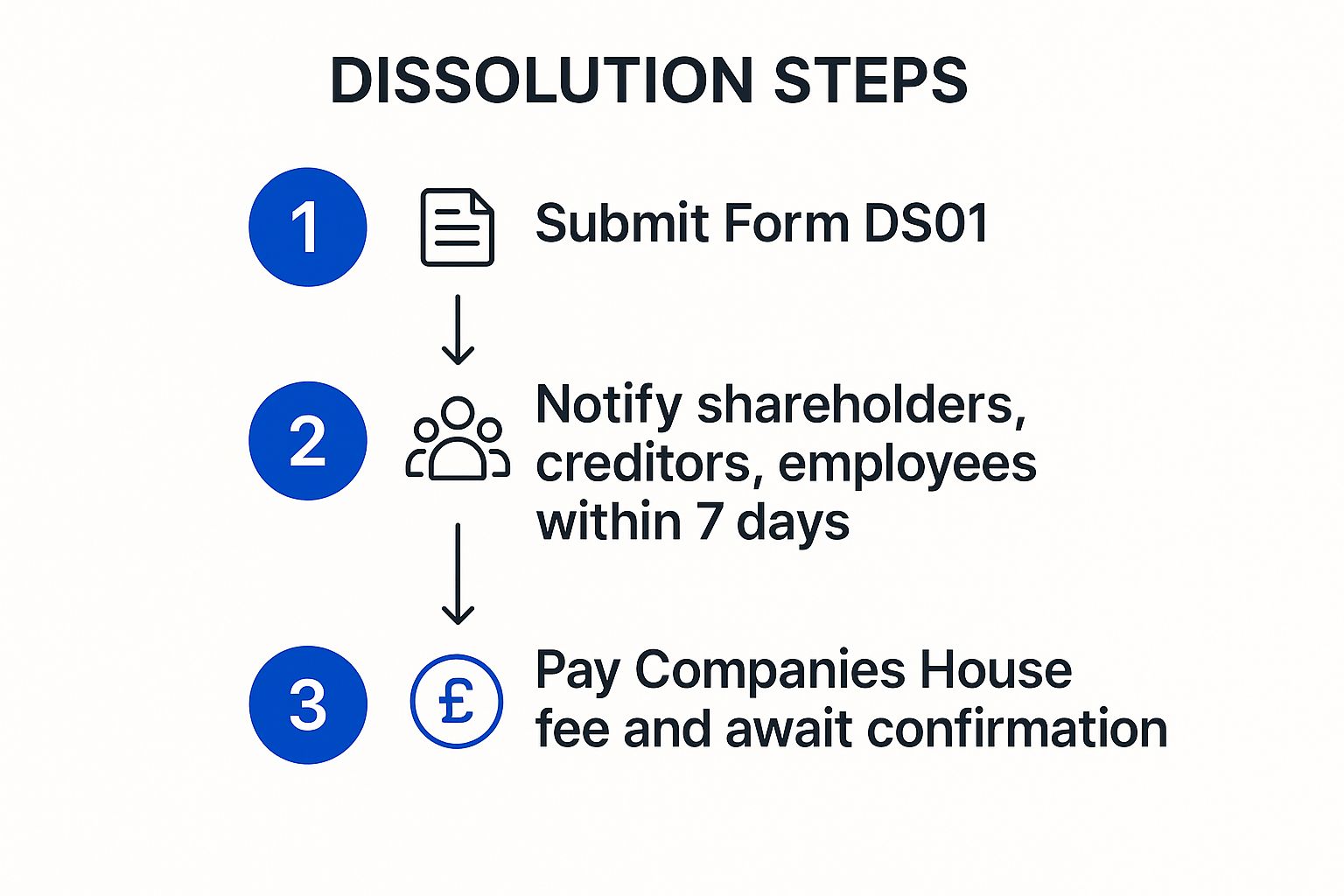

What are the key things to know about striking off? Well, first and foremost, your company needs to be dormant. This means it hasn't been trading or selling anything for at least three months. No business transactions, no dealing with customers, just… chilling. Also, and this is a biggie, your company must have no outstanding debts. This includes money owed to HMRC (Her Majesty's Revenue and Customs), suppliers, or anyone else. It’s like making sure you’ve paid for all your theatre tickets before you leave the show – no loose ends!

If your company meets these criteria, you can apply to strike it off the register. You’ll need to submit an application (form DS01, if you're curious) to Companies House. This whole process can take a few months. Companies House will usually publish a notice in The Gazette, which is the official public record, giving people a chance to object if they have a good reason. If there are no objections, poof! Your company is gone.

It's important to note that striking off is usually for smaller, simpler businesses that have ceased trading. If your company has assets or significant debts, this might not be the best route for you. It's best suited for those "gentle exit" scenarios.

2. Members' Voluntary Liquidation (The More "Formal" Farewell)

This is the more formal process, and it’s usually what you'd go for if your company is solvent (meaning it can pay all its debts) but you still want to wind it up. Think of this as a meticulously planned, grand send-off for your company. It's like orchestrating a beautiful retirement party where everyone gets their fair share and all the loose ends are tied up with a flourish.

In this process, a liquidator is appointed. This person is an insolvency practitioner, a professional who will oversee the winding up of your company. They'll be the conductor of this whole operation. Their job is to sell off any company assets, pay off any creditors (including HMRC), and then distribute any remaining money to the shareholders (that’s you and any other owners!).

This process can take a bit longer than striking off, and it involves more paperwork and professional fees. However, it’s the proper way to close a solvent company, especially if there are a few complexities, like assets to sell or a substantial amount of money to be distributed. It provides a level of certainty and assurance that everything has been handled correctly and legally.

There are different types of liquidation, but for a solvent company, it’s a Members' Voluntary Liquidation (MVL). The members (shareholders) of the company decide to wind it up. It’s a decision made by the owners to formally close the business in a controlled manner.

What About Company Debts?

This is a really crucial point. If your company owes money, you can't just pretend it doesn't exist. If you owe money and the company can't pay it, that’s when things get more complicated, and you might be looking at a Creditors' Voluntary Liquidation, which is a different kettle of fish altogether. But for the purposes of dissolving a solvent company, we’re focusing on paying everyone off!

So, before you even think about dissolving, get a clear picture of your company's financial situation. Are there any outstanding invoices? Any tax bills? Making sure all these are settled is paramount. It's like doing your homework before the big exam – you want to be prepared!

The Official Bit: Companies House

No matter which route you choose, you’ll be interacting with Companies House, the UK's registrar of companies. They are the official gatekeepers of company information. Think of them as the librarian of all company records in the UK. They need to know when your company is officially signing off.

For striking off, you’ll be sending them form DS01. For liquidation, the liquidator will be managing most of the communication with Companies House, but you'll still be involved in the initial decisions.

Is It Worth Doing It Properly?

Absolutely! Trying to avoid the formal process, or just letting a company sit there dormant for years without formally dissolving it, can lead to all sorts of headaches down the line. You might face penalties or fines, or it could even cause issues if you're trying to set up a new business in the future. It’s like trying to sweep dust under the rug; it just tends to reappear later, often making a bigger mess.

A proper dissolution ensures that your company is legally dissolved and no longer exists. This means you're no longer liable for its actions or debts. It’s a clean break, and that’s usually what everyone wants when they're moving on from a business venture.

The Takeaway

So, there you have it. Dissolving a company in the UK isn't some dark, mysterious art. It's a structured process with clear steps. Whether you're striking off a quiet company or going through a voluntary liquidation, it's all about bringing your business journey to a proper, legal close. It’s a chance to reflect on the good times, learn from the challenges, and then, with a clear conscience and a tidy record, embark on whatever exciting path lies ahead. Pretty cool, right?