How Much Should I Spend On Rent

Hey there, fellow humans navigating the wild and wonderful world of adulting! So, we're going to chat about something that pops up for pretty much everyone at some point: figuring out how much rent is actually okay to shell out each month. It sounds straightforward, right? But anyone who's ever stared at a lease agreement with wide, slightly panicked eyes knows it's a whole lot more nuanced than just picking a number.

Think of it like this: rent is kind of like that awesome pizza you're craving. You could go for the extra-large, loaded-up supreme, and hey, it'll be delicious! But then, there's no money left for, you know, other fun stuff. Or, you could grab a decent medium, and still have cash for that fancy craft beer you've been eyeing. It’s all about finding that sweet spot, isn’t it?

So, how do we even begin to untangle this rent riddle? Well, the first thing to remember is that there's no magic, one-size-fits-all answer. What works for your buddy who lives in a bustling city might be way too much for your cousin chilling in a quieter town. It’s like trying to tell everyone the "perfect" song to listen to – impossible!

Must Read

The "Rule of Thumb" and Why It's More Like a Suggestion

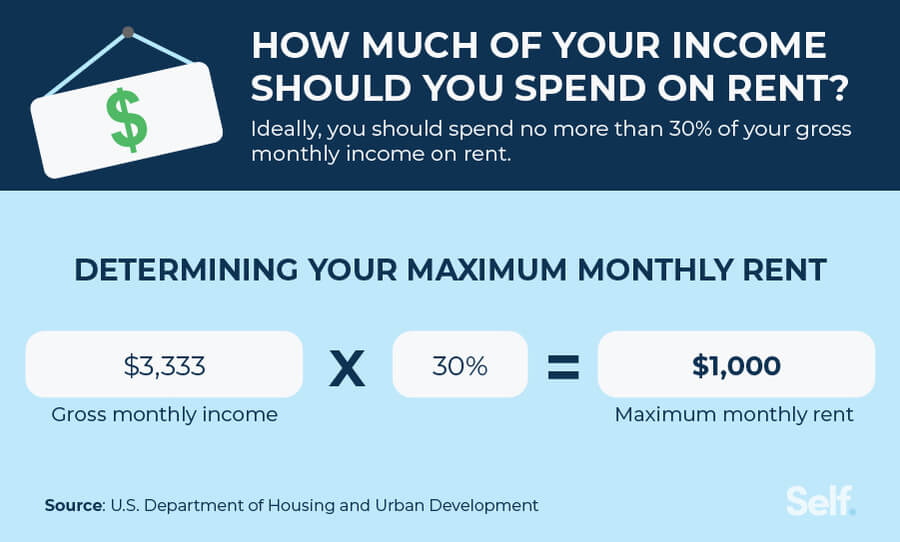

You’ve probably heard about the old "30% rule," right? The idea is to spend no more than 30% of your gross monthly income on rent. Sounds simple, even reassuring. It’s been around forever, like a comfy old armchair.

But here’s the tea: is it still the gold standard in today's world? For some, it’s a solid starting point, a helpful anchor. If you make, say, $5,000 a month before taxes, 30% is $1,500. That might be perfectly reasonable where you live. It leaves you with plenty of dough for groceries, utilities, and maybe even a Netflix subscription (because, priorities).

However, for others, especially in super expensive areas like San Francisco or New York City, that 30% might barely get you a closet with a window. In those cases, sticking to it could mean living on ramen noodles and wearing the same socks for a week (okay, maybe not that extreme, but you get the picture).

So, while it's a handy little guideline, it's more of a gentle nudge than a strict law. Think of it as the opening chapter of a book, not the whole epic saga.

Let's Talk About "Disposable Income" – The Fun Money Zone

This is where things get really interesting. Beyond just covering the basics, what do you actually want to do with your money? Do you dream of weekend getaways, collecting vintage vinyl, trying out every new restaurant in town, or saving up for that epic travel adventure?

Your rent payment significantly impacts that “fun money” zone, also known as your disposable income. If your rent eats up a huge chunk, your ability to do those other awesome things shrinks right along with it. It’s like having a giant, hungry monster that just swallows all your fun.

Imagine you have $2,000 left after taxes. If rent is $1,800, yikes. That leaves only $200 for everything else – food, bills, entertainment, clothes, everything. Now, if rent is $1,000, that leaves you with a much healthier $1,000 for the rest of your life. See the difference? It’s not just about survival; it’s about thriving and having some wiggle room.

Figuring Out Your Personal Rent Sweet Spot

So, how do we find your sweet spot? It’s a bit of detective work, really. First, let’s get real about your actual take-home pay. That’s the money that hits your bank account after taxes, health insurance, and any other deductions. This number is your best friend for budgeting.

Next, list out all your essential monthly expenses. Think:

- Groceries

- Utilities (electricity, gas, water, internet – the necessary evils)

- Transportation (car payments, gas, public transport passes)

- Student loan payments

- Insurance (health, car, renters)

- Minimum debt payments

Once you’ve tallied those up, subtract that total from your take-home pay. What’s left? This is your disposable income.

Now, consider your financial goals. Are you trying to:

- Build an emergency fund (super important, like a financial superhero cape)?

- Save for a down payment on a house?

- Pay off debt aggressively?

- Invest for the future?

- Travel the world?

See how rent plays a role in all of these? If your rent is too high, those goals might feel like climbing Mount Everest in flip-flops. You need to find a rent that allows you to also put money towards the things that matter to you long-term.

The "Cost of Living" Factor – It's a Biggie

Let's be honest, the cost of living in different places is wildly different. A studio apartment in a major metropolitan hub can cost more than a three-bedroom house in a smaller city. It’s like comparing the price of a single truffle to a whole box of chocolates – they're both sweet, but the scale is different!

If you live somewhere with a high cost of living, you might have to accept that a larger portion of your income will go towards rent. That’s just the reality. In this scenario, you'll need to be extra savvy with your other expenses. Maybe that means cooking at home more, finding free or low-cost entertainment, or being super mindful of your shopping habits.

Conversely, if you're in a more affordable area, you have more freedom! You might be able to spend less on rent and put more towards savings, travel, or hobbies. It’s all about playing the game with the cards you’ve been dealt, right?

What If You're Sharing the Rent Load?

Ah, roommates! The age-old solution to making rent more manageable. Sharing a place can significantly reduce your individual rent burden. This is a fantastic way to free up cash for other things.

When you have roommates, your rent percentage might look much lower than if you were living solo. This can feel like winning the lottery! However, remember to factor in shared utilities and potential disagreements over household stuff (who bought the toilet paper this time?).

The key with roommates is open communication. Discuss finances openly, agree on bills, and set expectations. A good roommate situation can make your housing costs much more comfortable and leave you with more money for, well, everything else!

The "Comfort Level" – It's More Than Just Numbers

Beyond the math, there’s a very real feeling associated with your rent. Do you feel constantly stressed about making rent? Are you dreading the first of the month? If so, your rent might be too high, even if it technically fits some rule.

Your home should be a sanctuary, not a source of constant anxiety. If paying rent leaves you feeling financially squeezed and stressed, it’s probably time to reconsider your living situation. That peace of mind is priceless.

On the flip side, if you can comfortably afford your rent and still have money for savings, fun, and the occasional splurge, you're likely in a good place. It’s about feeling secure and having the freedom to enjoy your life.

So, What's the Verdict?

Ultimately, the "right" amount to spend on rent is highly personal. It depends on your income, your location, your essential expenses, your financial goals, and your overall comfort level.

Instead of a rigid rule, think of it as a flexible guideline. Start with that 30% idea, but then dig deeper. Understand your own finances, what you value, and what you want your money to do for you. Are you willing to make sacrifices in other areas to live in a certain neighborhood? Or is having more disposable income a higher priority?

Don't be afraid to play around with a budget. There are tons of apps and spreadsheets that can help. Play the "what if" game. What if rent was $100 less? What would you do with that extra $100? What if it was $200 more? How would that impact your goals?

Finding the right rent is a balancing act, a bit like juggling flaming torches (but way less dangerous, hopefully!). It’s about making informed decisions that align with your life, your dreams, and your wallet. And hey, when you get it right, you’ll have more freedom to do all the cool stuff life has to offer!