How Much Money To Retire At 55

So, you're dreaming of trading in your alarm clock for an alarm of birds chirping? Retiring at 55 sounds like a fantastic plot twist in the story of your life! But the big question, the one that might have your brain doing a little jig, is: how much money do you actually need? It’s a number that can feel as elusive as a unicorn, but let's break it down, shall we?

Think of it like planning a really epic vacation. You wouldn't just show up at the airport with a vague idea of where you're going, right? You need a budget! This retirement thing is kind of the same, just a much, much longer vacation. And trust me, the destinations are even better!

The first big thing to consider is your lifestyle. Are you picturing yourself lounging on a beach with a fancy cocktail? Or maybe you're more of a "hike every day" kind of adventurer? Your retirement dreams directly impact your dollar dreams. What does your ideal day look like, post-work?

Must Read

Let's get a little more specific. Imagine you're living a pretty comfortable life right now. Many experts suggest aiming to replace about 70% to 80% of your current income in retirement. This isn't a hard and fast rule, but it’s a great starting point for your money calculations.

Why that percentage? Well, a few things might change. Maybe your commute costs disappear, those work clothes might not be needed as often, and perhaps you'll be able to pay off your mortgage before you hang up your hat. These are all glorious money-saving victories!

However, some expenses might actually increase. Healthcare costs can be a big one, and you might find yourself wanting to travel more or pick up new hobbies that cost a little cash. It's all about balancing the savings with the new adventures.

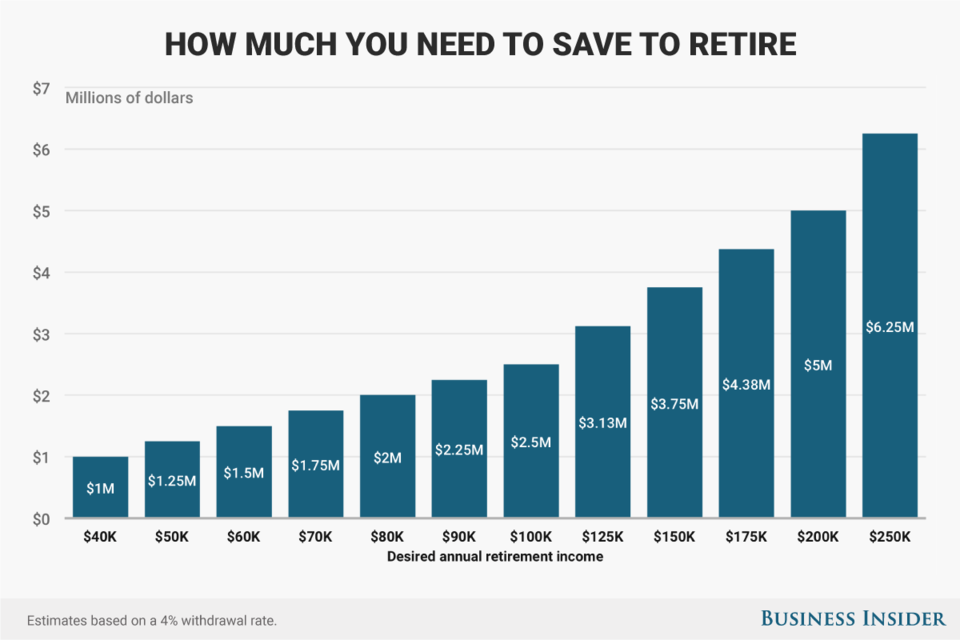

Now, let's talk about the magic number. This is where things get really exciting. While there's no single answer that fits everyone like a glove, a common benchmark tossed around is the $1 million mark. Yes, a million dollars sounds like a lot, and it is! But for retiring at 55, it’s a number that offers a comfortable runway.

This isn't just a random number pulled out of a hat. It’s based on a few key financial principles. One of the most famous is the "4% rule". It suggests you can safely withdraw about 4% of your retirement savings each year, and your money should last for roughly 30 years.

So, if you have $1 million saved, that means you could potentially spend $40,000 a year. For many people, this is a very livable amount, especially if they’ve paid off their home and have other income streams. It's like having a generous allowance from your future self!

But here's the fun part: what if you can’t quite hit that $1 million target? Don't despair! That's the beauty of planning. You can adjust. Maybe your ideal retirement involves a slightly less extravagant lifestyle, or perhaps you have other income sources that can fill the gap.

Consider things like Social Security. While you can claim it earlier, waiting until closer to your Full Retirement Age (which is usually 67) means a bigger monthly check. This can significantly boost your retirement income, making that $1 million goal less daunting.

What about part-time work? Many people retiring at 55 don't want to stop working entirely. They might choose to do something they love on a less intense schedule. This could be anything from consulting to pursuing a passion project that brings in a little extra cash. It’s like a fun side hustle for the retired!

The key here is to get a crystal-clear picture of your expenses. Track every single dollar you spend for a month or two. It’s eye-opening, and honestly, a little bit like a detective mission for your own finances. Where does your money go?

Once you know your spending habits, you can start projecting. How much will your grocery bill be? How much do you anticipate spending on travel, hobbies, or unexpected fun? This is where your retirement spreadsheet, or perhaps a friendly financial advisor, can become your new best friend.

Let's talk about healthcare. This is a big one, especially for those retiring before Medicare eligibility at 65. You'll need to factor in the cost of health insurance, which can be a significant expense. Researching options like the Affordable Care Act (ACA) marketplace is a smart move.

Don't forget about inflation. The cost of things tends to go up over time. That $10 cup of coffee today might be $15 in 20 years. Your retirement nest egg needs to be able to grow and keep pace with these rising costs. This is where smart investing comes into play.

Speaking of investing, how are your savings structured? Are they in 401(k)s, IRAs, or other investment accounts? The types of accounts you have and how your money is invested will significantly impact its growth potential. This is the engine that can make your money work for you!

Retiring at 55 often means you'll need your money to last longer than someone retiring at 65 or 70. This is why having a solid plan and potentially a larger savings amount is crucial. It’s about building a financial foundation that can support your dreams for decades to come.

Consider the "bucket strategy". This is a fun way to visualize your retirement funds. You might have one bucket for immediate expenses (cash), another for growth (stocks), and a third for income (bonds). It helps you manage your money and feel more secure.

Another thought is to look at your debt. Ideally, you want to be debt-free before you retire. Carrying a mortgage or other loans into retirement can put a serious strain on your budget. Paying these off is like giving your retirement income a significant boost!

What about longevity? We're living longer, which is fantastic news! But it also means your retirement savings need to stretch further. Planning for a 30-year retirement is good, but what if you live to 90 or even 100? It's a happy problem to have, but one that requires careful planning.

So, while the $1 million figure is a common starting point, the real answer is deeply personal. It’s about understanding your unique circumstances, your spending habits, and your retirement aspirations. It’s a puzzle, and you get to put the pieces together!

The most important thing is to start planning early. The sooner you begin saving and investing, the more time your money has to grow. Even small, consistent contributions can make a huge difference over time. It’s like planting a money tree!

Don't be afraid to seek professional advice. A good financial advisor can help you create a personalized retirement plan, assess your risk tolerance, and make sure you're on the right track. They’re like your financial GPS, guiding you to your retirement paradise.

Retiring at 55 is absolutely achievable and can be an incredibly rewarding chapter of your life. It’s about taking control of your finances and designing the retirement you’ve always dreamed of. It's your adventure, and the budget is your map!

So, take a deep breath, grab a pen and paper (or your favorite budgeting app), and start crunching those numbers. The journey to your dream retirement at 55 begins now, and it’s going to be one heck of a ride!