How Do You Make A Trust Fund

Ever find yourself scrolling through Insta, catching glimpses of those effortlessly chic lives – the European vacations, the spontaneous art purchases, the general vibe of "money? what money?" It's easy to daydream about a life where financial worries are a distant echo, or better yet, a forgotten concept. And often, lurking in the background of these perfect snapshots is the magic ingredient: a trust fund.

Now, before your eyes glaze over with visions of dusty legal documents and complex financial jargon, let's take a deep breath. Creating a trust fund isn't some exclusive club for billionaires. While it certainly can be a very sophisticated tool for the ultra-wealthy, the underlying principles are accessible, and the idea of a trust fund can be a brilliant way to secure the future, whether for yourself, your kids, or even a beloved (and surprisingly expensive) poodle.

So, What Exactly Is a Trust Fund, Anyway?

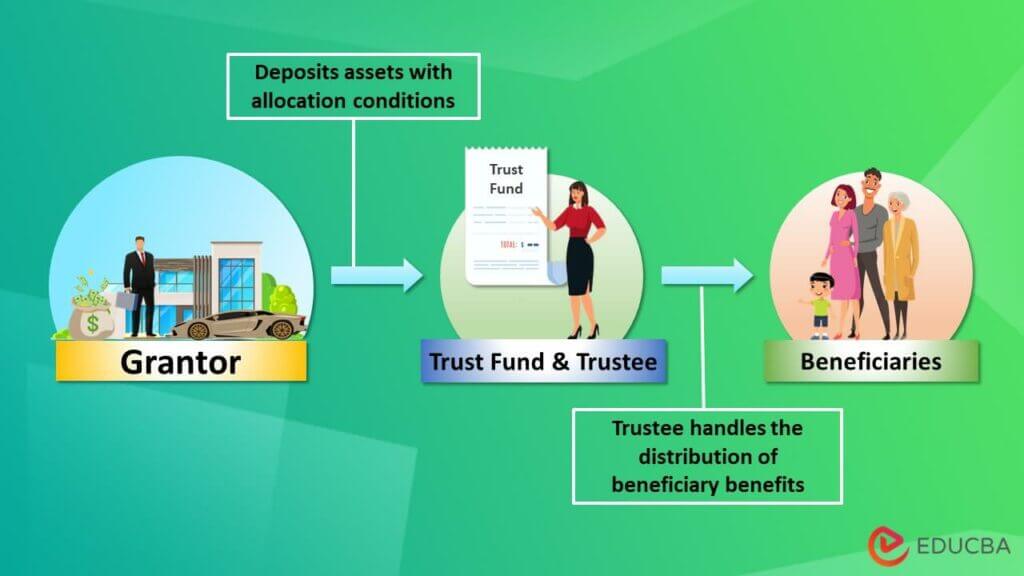

Think of it like a special financial piggy bank, but way cooler and with way more rules. In its simplest form, a trust is a legal arrangement where one person (the grantor, aka the one setting it up) gives assets to another person (the trustee) to hold and manage for the benefit of a third party (the beneficiary).

Must Read

The "fund" part just means the assets being held are usually investments, real estate, or other valuable stuff. It's not just cash sloshing around; it's a carefully curated pot of wealth designed to grow and be distributed according to the grantor's wishes.

Why Bother? The Sweet, Sweet Benefits

Okay, so why go through the hoops? Well, trust funds offer some pretty compelling advantages:

- Control: This is huge. You get to dictate exactly how and when your assets are used. Want your grandkids to use it for education only? Boom. Need to ensure your future self has a comfortable retirement, no matter how many impulsive sourdough starter kits you buy? Done.

- Privacy: Unlike a will, which becomes a public record after your death, trusts are generally private. So, your family's financial dealings can remain, well, family business. Think of it as the Champagne of estate planning – bubbly, exclusive, and not for everyone to sip.

- Avoiding Probate: This is the legal process of validating a will and distributing assets. It can be time-consuming, expensive, and frankly, a bit of a drag. Trusts bypass probate, meaning your beneficiaries can get their inheritance much faster and with fewer headaches. It's like having a VIP express lane for your wealth.

- Asset Protection: Depending on the type of trust, it can offer a shield against creditors or lawsuits. Imagine a financial force field for your hard-earned money.

- Special Needs Planning: For beneficiaries with disabilities, a carefully crafted special needs trust can ensure they receive financial support without jeopardizing their government benefits. It's a thoughtful and compassionate way to provide for loved ones.

Let's Get Down to Business: How Do You Actually Make One?

Alright, so you're intrigued. You're picturing that little piggy bank, but a really sophisticated one. Here's the general roadmap:

Step 1: Dream Big (and Be Specific!) – Define Your Goals

Before you even think about lawyers, grab a latte and a notebook. What do you want this trust to do? Who is it for? When should they benefit? What kind of assets do you envision going into it?

Are you thinking about:

- Funding your children's college education?

- Providing a safety net for a spouse?

- Ensuring a beloved pet lives out its days in luxury (complete with a dedicated groomer)?

- Leaving a legacy for a favorite charity?

- Setting up something for your future self – because, let's be honest, retirement sounds pretty good.

The more clarity you have, the easier the next steps will be. Think of it like planning a killer playlist – you need to know the vibe you're going for before you start picking songs.

Step 2: Choose Your Champion – The Trustee

This is a crucial role. The trustee is the one who will manage the trust assets and make distributions according to your instructions. They need to be responsible, trustworthy, and financially savvy. They also need to understand your wishes.

You can appoint:

- An individual: This could be a trusted family member, a close friend, or even yourself (in some types of trusts during your lifetime). Key consideration: Are they up to the task? Do they have the time and expertise?

- A professional trustee: This could be a bank's trust department or an independent trust company. They have the professional experience and are bound by fiduciary duties. Think of them as the "suits" who know their stuff.

A fun fact: Sometimes, you can appoint a co-trustee, like a family member and a professional, to get the best of both worlds – personal oversight and expert management.

Step 3: Pick Your Perfect Partnership – The Type of Trust

This is where things get a little more technical, but don't panic. There are two main categories:

Revocable Trusts: The Flexible Friends

With a revocable trust, you can change, amend, or even dissolve it during your lifetime. You, as the grantor, typically maintain a lot of control. This is often used for avoiding probate and managing assets during your lifetime. Think of it as a really fancy, customizable wallet that you can open and rearrange as you please.

Irrevocable Trusts: The "Set It and Forget It" (Kind Of)

Once created, these trusts are generally permanent. You can't easily change them. This type of trust is often used for more advanced estate planning, such as reducing estate taxes or protecting assets from creditors. It's like sealing a beautifully preserved time capsule – once it's closed, it's meant to last.

Within these broad categories, there are many specific types of trusts, like:

- Living Trusts (Inter Vivos Trusts): Created and funded during your lifetime.

- Testamentary Trusts: Created by your will and only come into effect after your death.

- Charitable Trusts: Designed to benefit a charity.

- Special Needs Trusts: For beneficiaries with disabilities.

Pro Tip: This is where a good estate planning attorney is your absolute best friend. They'll help you navigate the options and pick the one that aligns perfectly with your goals. It's like a stylist for your financial future!

Step 4: Assemble Your Dream Team – Hire an Attorney

Seriously, you can't skip this. While you can get the idea of a trust fund, actually drafting the legal documents requires expertise. An estate planning attorney specializes in this stuff. They'll understand your goals, explain the legal implications, and draft a trust document that is legally sound and perfectly tailored to your needs.

Think of them as the architects of your financial legacy. They'll ensure every beam is strong and every room is exactly where you want it. Plus, they can help you avoid common pitfalls that could unravel your carefully laid plans.

Step 5: Fund the Future – Transfer Your Assets

Once the trust document is signed and finalized, you need to transfer your assets into it. This is called "funding the trust."

This might involve:

- Changing the title of real estate from your name to the trust's name.

- Transferring brokerage accounts to the trust.

- Assigning ownership of life insurance policies.

Your attorney and potentially a financial advisor will guide you through this process. It's like decorating your new house – the structure is there, now it's time to fill it with your treasures.

Step 6: Keep It Alive and Well – Ongoing Management

A trust isn't a "set it and forget it" thing in the absolute sense (unless it's a very simple testamentary trust). The trustee will need to manage the assets, keep records, file taxes (if applicable), and make distributions according to the trust's terms. Regular reviews with your attorney and trustee are a good idea to ensure the trust continues to meet your evolving needs.

Fun Little Facts to Impress Your Friends (or Just Yourself!)

- The concept of trusts can be traced back to ancient Roman law, where it was known as fideicommissum. Talk about old-school wealth management!

- Some trusts are specifically designed to hold art collections or intellectual property. Imagine a trust dedicated to ensuring your legendary cookie recipes are passed down through generations!

- The world's largest trust fund is rumored to be worth hundreds of billions of dollars. That's a lot of lattes.

- You can even set up a trust for your pet! Yes, your furry (or scaly, or feathered) friend can have a dedicated fund for their care.

A Daily Dose of Trust

Thinking about trust funds might seem like a grand, far-off concept, but the underlying idea – planning for the future and ensuring security – is something we all do in smaller ways every day.

When you set aside money in a savings account for a rainy day, you're engaging in a basic form of future financial security. When you make a will, you're planning for the orderly distribution of your belongings. These are all building blocks of responsible financial stewardship.

Creating a trust fund is simply taking that concept to a more formal, sophisticated level. It’s about extending your care and foresight beyond your own immediate needs, creating a lasting positive impact for those you love. It’s a way to say, "I've got you, even when I can't be there." And in a world that can sometimes feel a bit chaotic, that kind of peace of mind is truly priceless.