How Do I Get A Pension Forecast

Hey there, coffee buddy! So, you're wondering about getting a pension forecast, huh? Like, what's that even about and how do you actually do it? Don't worry, you're not alone. This whole pension thing can feel like a secret club, can't it? But guess what? It's totally accessible, and getting a forecast is your first step to actually understanding what you're working with for your golden years. Let's spill the beans, shall we?

Think of a pension forecast like a sneak peek into your future financial self. It’s not some crystal ball, mind you, but it’s pretty darn close to knowing how much lovely cash you might be able to sip your retirement cocktails with. It's essentially a projection, an educated guess, if you will, based on your current contributions and how your investments are supposed to perform. Pretty neat, right?

So, why bother, you ask? Well, let me tell you, ignoring it is like playing financial hide-and-seek with yourself. You don't want to be that person who suddenly realizes in their 70s that their retirement fund is… well, let's just say a bit sparse. A forecast helps you avoid that awkward moment. It gives you a clear picture, so you can make informed decisions now, while you still have time to, you know, do something about it. It’s all about being proactive, my friend. Be a pension superhero, not a retirement worrier!

Must Read

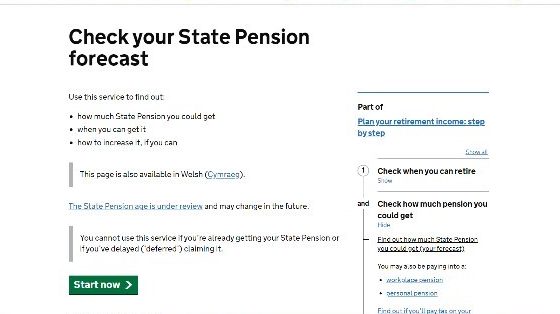

Alright, let's get down to the nitty-gritty. How do you actually get your hands on this magical forecast? It really depends on where your pension is. You see, pensions aren't one-size-fits-all. They come in different flavors. Are you talking about a workplace pension? A personal pension? Maybe you've got one from a previous job that you've forgotten about? Each one has its own path to a forecast.

Let's start with the most common one: your workplace pension. If you're employed, chances are your employer is already contributing to a pension for you. They're the good guys! This is often called a "defined contribution" scheme, which means the amount you get depends on how much is paid in and how well the investments do. Sounds familiar, right? So, to get a forecast from your workplace pension, you usually just need to contact your HR department or your pension provider directly. They'll have all the information. Easy peasy, lemon squeezy!

Sometimes, your employer will have a dedicated portal or website for your pension. It’s like a little online hub where you can see your contributions, investment performance, and, voilà, your pension forecast! Log in, poke around a bit, and you should find it. If you're drawing a blank, don't be shy. Send an email. Make a call. They're paid to help you with this stuff, so use them!

Now, what if you've switched jobs a few times? Don't panic! It's super common to have a few old pensions lurking around. These are often called "deferred" pensions. You're not actively contributing to them anymore, but the money is still there, hopefully growing. For these, you'll need to track down the pension provider from when you worked at that company. Remember that old company name? Good! Then you can try searching online for that provider. Most providers have websites where you can log in to your old account or request a statement, which will include a forecast. It might take a bit of detective work, but think of it as a treasure hunt for your future self!

If you're struggling to find old pension providers, there's a superhero in town: the Pension Tracing Service. Yep, the government offers this free service! You give them details of past employers, and they'll try to find your lost pensions. How amazing is that? It's like a reunion for your forgotten retirement funds. Just search for "Pension Tracing Service" online, and you'll find their website. Fill in the form, and let them do their magic. It’s a lifesaver for those pensions you’ve completely lost track of.

Then there are personal pensions. These are ones you set up yourself, outside of your employer. Maybe you're self-employed, or you just wanted to top up your workplace pension. These are usually managed by investment companies or financial advisors. To get a forecast here, you'll be dealing directly with your pension provider (the company you set it up with). They'll have an online portal, or you can contact their customer service. They'll be able to give you an up-to-date statement with a projection of your retirement income. It's pretty straightforward if you know who you set it up with.

Okay, so you’ve found your pension provider(s). What happens next? Usually, you’ll log into your online account. Look for a section that says "Your Retirement Income," "Pension Forecast," or something similar. It might be under "Statements" or "Projections." Sometimes, they'll send you an annual statement automatically, and that will often contain a forecast. Keep an eye out for those in the mail or your inbox!

If you can't find it online, don't fret. Most pension providers have a customer service helpline. Give them a ring! They're there to assist you. Explain that you're looking for a pension forecast. They might ask you a few security questions to confirm your identity – you know, the usual stuff. Then, they'll either guide you to it online or send you a physical copy by post. It’s always a good idea to have a pen and paper handy when you call, just in case they give you some numbers or important details you’ll want to jot down.

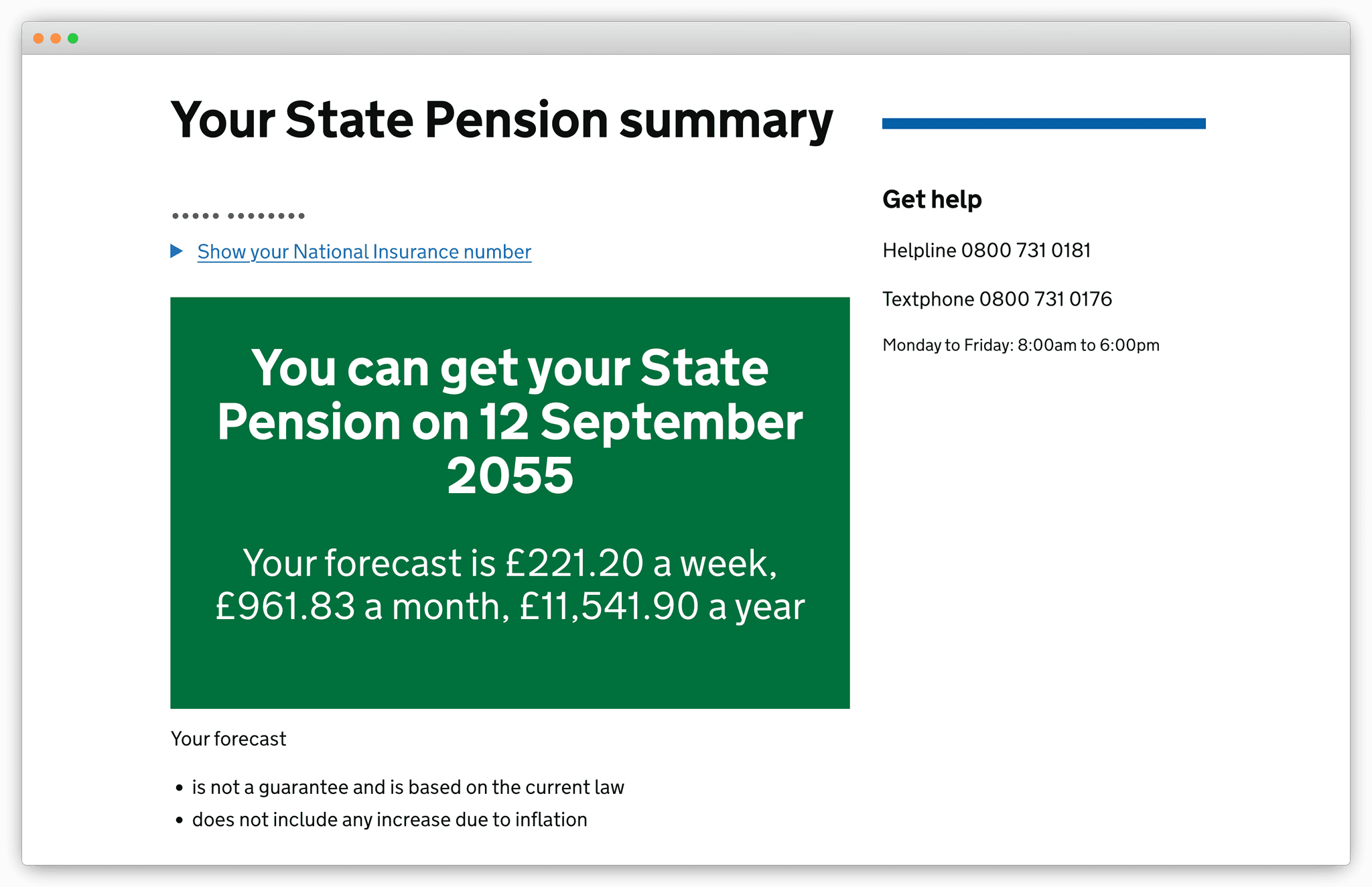

When you get your forecast, don't just glance at it and toss it aside. Take a moment to actually understand it. It will usually show you an estimated annual income, broken down into weekly or monthly figures. It might also give you a lump sum option, if that's something your pension plan allows. Crucially, these forecasts are usually based on certain assumptions. They might assume a certain rate of investment growth, and they might assume you'll continue contributing until a certain age. It’s important to read the small print (yes, I know, the dreaded small print!) to see what those assumptions are.

For example, a forecast might say, "Assuming 5% annual investment growth and you retire at 65." If you’re planning to retire later, or if you think the market might be a bit more… excitable than that, your actual outcome could be different. So, think of the forecast as a baseline, a starting point for your financial planning. It's not set in stone, but it's a darn good indicator.

Now, a word to the wise: if you have multiple pensions, it can be a bit of a headache to collate all those forecasts into one big picture. You'll want to add up all those estimated annual incomes to get a rough idea of your total retirement income. This is where a bit of spreadsheet wizardry might come in handy, or if you’re feeling fancy, a financial advisor can help you consolidate all of this information and give you a more holistic view.

What if your forecast looks… a little less than exciting? Don't despair! This is precisely why you got the forecast in the first place. It gives you the opportunity to make changes. Can you increase your contributions? Can you review your investment choices to see if there's a better fit for your risk tolerance and goals? These are all questions you can explore. Your pension provider often has tools or information on their website to help you with this, or again, a chat with a financial advisor can be super beneficial here.

And hey, remember that there are other sources of income in retirement besides your pension. You might have savings, investments, property, or even expect some inheritance. The pension forecast is just one piece of the retirement puzzle. It’s a big piece, mind you, but still a piece.

Some people might choose to get a pension forecast from a financial advisor. This can be a great option if you have complex finances, multiple pension pots, or if you just want a professional opinion. An advisor can not only get your forecasts but also help you understand them in the context of your overall financial situation and retirement goals. They can also advise you on how to potentially increase your retirement income. Just be aware that financial advisors usually charge a fee for their services, so it’s worth shopping around and understanding their fee structure.

The important thing is to take action. Don't let the fear of what you might find stop you from looking. Knowledge is power, especially when it comes to your future financial well-being. So, grab that cuppa, find your pension provider’s details, and get that forecast. You'll thank yourself later, trust me. It's your future, and it's worth investing a little time to understand it!

So, to recap: for workplace pensions, contact your HR or pension provider. For old pensions, use the Pension Tracing Service or contact the providers directly. For personal pensions, go straight to your provider. Look for "forecast," "projection," or "retirement income" on their website or in your statements. Don't be afraid to call them. And when you get it, actually read it and understand the assumptions. This is your financial future we're talking about, after all!

It’s not rocket science, but it does require a little bit of effort. But think of the peace of mind you’ll gain. No more wondering if you'll be living on beans on toast in retirement (unless you like beans on toast, of course!). You’ll have a much clearer picture, and that’s priceless. So, go forth, my friend, and conquer your pension forecast!