Does In Credit Mean I Owe Money

You know, I was at that awkward phase the other day, the one where you're trying to pull out your wallet, simultaneously juggling a coffee, your phone, and a runaway umbrella that's decided it wants to explore the sidewalk. As I fumbled for my card at the checkout, the cashier cheerfully chirped, "Oh, you've got credit on this!" My brain did a little stutter. Credit? Me? Does that mean I actually owe someone money? Or is it like a bonus, a little pat on the back for being such a good shopper?

It's funny how those little phrases get thrown around, isn't it? They feel so familiar, so everyday, yet when you stop and actually think about them, they can be surprisingly confusing. "Credit" is one of those words. We hear it all the time. "Build your credit." "Good credit score." "Credit card." But what does it really mean, especially when someone says you have it? Let's dive into this little linguistic puzzle, shall we? Because, spoiler alert, it's not always as straightforward as it seems.

So, When Someone Says "You've Got Credit," What Do They Mean?

Okay, let's break it down. In the most common everyday context, when a cashier or a shop assistant says, "You've got credit on this," they're usually referring to a positive balance on a pre-paid card, a gift card, or sometimes even a store account where you've overpaid. Think of it like this: you've handed over more money than you actually needed to spend. So, instead of getting cash back (which can be a hassle), they're saying, "Hey, you've got a little stash of money waiting for you here."

Must Read

It's like when you return something to a store, and they offer you store credit. You didn't get your cash back, but you have the right to purchase something else from them with that amount. Pretty neat, right? It means you don't owe them, they owe you the value of that credit. So, in this scenario, you do NOT owe money. Quite the opposite, actually!

This is the most common scenario you'll encounter in a retail setting. You bought something, paid for it, maybe returned it, or perhaps you topped up a gift card with a bit extra. The shop then owes you that extra bit. It's essentially money you've already paid, held by the merchant for your future use. Easy peasy.

But Wait, There's More! The Slippery Slope of "Credit"

Now, here's where things can get a little... well, credit-y. The word "credit" is a chameleon. It can mean a lot of different things depending on the context. And sometimes, the way people use it can make you scratch your head. We've covered the "positive balance" kind of credit, which is lovely. But there's another, much more common, interpretation that involves owing money. Gasp!

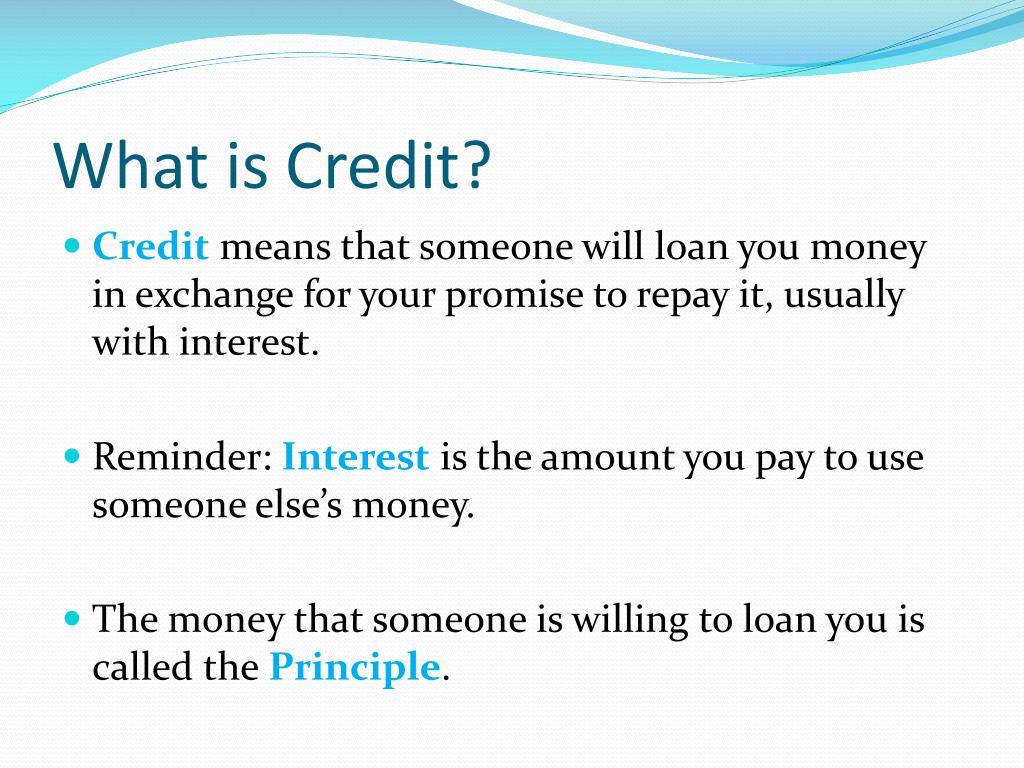

Think about your credit card. When you use it, you're essentially borrowing money from the credit card company. That's credit in the sense of being granted the ability to borrow. You're not paying for it immediately. The credit card company is extending you credit, meaning they are trusting you to pay them back later. So, every swipe, every tap, every online purchase using your credit card is a form of debt you're accumulating.

And that, my friends, is where the "owing money" part comes in. When you use your credit card, you are, in essence, getting credit from the bank. This credit allows you to make purchases now, but you are obligated to repay that borrowed money, usually with interest, by a certain date. So, in this instance, yes, you do owe money.

It’s like being handed a blank check with a promise to fill it in with your own money later. The bank is saying, "Here, take this money, use it, and we'll send you a bill." And that bill is what you need to pay to clear your debt. This is the fundamental concept of borrowing money.

The Two Flavors of Credit: A Little Analogy

Let's try an analogy to make this crystal clear. Imagine you're at a potluck dinner.

Scenario 1: The "You've Got Credit" Scenario (Positive Balance)

You brought a massive, delicious lasagna. Everyone loves it. The host says, "Wow, thanks! You've put a lot of credit into this meal!" In this case, your lasagna is like a pre-paid item. You've already contributed. The host (or the store) owes you appreciation, and in the retail world, that's translated into a positive balance or store credit. You are owed. You don't owe anyone a slice of your lasagna; you've already given it.

Scenario 2: The "Credit Card" Scenario (Borrowing)

Now, imagine the host says, "Hey, there's not enough dessert! Can someone spot us for some ice cream, and we'll pay you back tomorrow?" If you lend them $10 for ice cream, you've extended them credit. They owe you $10. This is like using your credit card. You're getting the ice cream now (making the purchase), but you have a future obligation to repay the $10. The ice cream shop got paid by the credit card company, and now the credit card company wants their money back from you.

See the difference? In the first, you're owed. In the second, you owe. It all hinges on whether you’ve given something of value (money) that the other party is holding for you, or if you’ve received something of value that you’ve promised to pay for later.

Why Does This Distinction Matter So Much?

Well, aside from the fact that it can prevent you from walking away from a purchase with a confused look on your face (been there!), understanding this distinction is crucial for your financial health. It's about knowing whether you're spending money you already possess or money you're borrowing.

When you have a positive balance on a gift card or a store credit, it's a good thing! It means you have funds available. There's no pressure, no interest, just money you're entitled to use. It's like finding a forgotten fiver in your old jeans – a little win!

On the other hand, when you're using credit from a credit card, loan, or other forms of borrowing, you're entering into a contract. You're agreeing to a repayment schedule, and often, to interest charges. This is where responsible financial management comes into play. It's about understanding your limits, making payments on time, and not overspending on borrowed money.

Ignoring the fact that you owe money when using credit is a fast track to financial trouble. Those little monthly statements can quickly escalate into a mountain of debt if not managed carefully. This is why credit scores are so important. They reflect how well you've managed the credit you've been given in the past.

Common Scenarios Where "Credit" Can Be Confusing

Let's get real and talk about some everyday situations where this can pop up:

Gift Cards and Store Credit

This is where the "you have credit" usually means a positive balance. You bought a $100 gift card for $100. You've spent $30 on an item. The card now has $70 of credit on it. The store owes you $70 of merchandise. You do not owe them. Phew! This is the good kind of credit.

Or, you returned an item that was on sale, and the store policy is to give store credit instead of a cash refund. That store credit represents money you are owed by that specific store. Again, you don't owe money; the store owes you the value of that credit.

Pre-paid Phone Plans or Services

Some services, like certain phone plans, operate on a pre-paid basis. You load money onto your account, and then you use that money for calls, texts, or data. If you have "credit" on your phone account, it means you've pre-paid for the service. You do not owe the phone company money; they owe you the service for the credit you've added.

Credit Cards and Loans (The Other Side of the Coin)

This is where the "credit" means you've borrowed. When you open a credit card, the bank extends you a line of credit. This is the amount of money they are willing to lend you. Every purchase you make reduces that available credit and increases the amount you owe. So, if you have a $1000 credit limit and you've spent $500, you have $500 of credit available to borrow, and you owe $500.

Loans, whether it's a car loan, a mortgage, or a personal loan, are all about borrowing money. The bank or lender gives you a lump sum (the credit), and you agree to repay it over time with interest. You absolutely owe money in these situations.

The Irony of It All

It's quite ironic, isn't it? The same word, "credit," can mean you're owed money or you owe money. It's a linguistic tightrope walk. And in our daily lives, we navigate this without even thinking, most of the time. But it's these moments of pausing, of questioning, that can really solidify our understanding of financial concepts.

It's like the difference between having a full piggy bank (positive credit) versus a credit card bill (negative credit, or debt). Both involve the concept of "credit," but the implications for your wallet are vastly different. One is a source of funds; the other is a future obligation.

So, next time someone mentions "credit," take a second. What's the context? Are they talking about money you've already paid and is waiting for you, or money you've borrowed and need to pay back? Your bank account (and your stress levels) will thank you for it.

It's a good reminder that language is fluid and often context-dependent. And in the world of finance, understanding those nuances can save you a lot of headaches, or even better, save you some money. So, go forth and be credit-savvy, my friends!