Corelogic Opt Out Security Freeze

Hey there, lovely people! Let’s chat about something that sounds a bit… well, “corporate” at first glance, but trust me, it’s as important as remembering your spouse’s birthday or where you put your keys. We’re talking about your personal information, specifically how to keep it safe from folks who shouldn't be peeking. Today’s spotlight is on something called a CoreLogic Opt Out Security Freeze. Now, before you imagine a chilly ice block and a stern-faced security guard, let’s break it down in a way that’s as comfy as your favorite armchair.

Think of your personal data like your prized cookie recipe. You wouldn’t just hand it out to anyone, right? You guard it, maybe you even have a special, slightly smudged card where it’s written. Well, your Social Security number, your date of birth, your address – that’s like the secret ingredient to your amazing chocolate chip cookies. And unfortunately, there are some sneaky characters out there who would love to get their hands on it, not to bake cookies, but to open credit cards, take out loans, or generally cause mischief in your name. Yikes!

This is where our friend, the CoreLogic Opt Out Security Freeze, comes to the rescue. It’s not a literal freeze that’ll make your hands numb. Instead, it's more like putting up a really strong, invisible velvet rope around your credit information. This rope says, “Hold on a minute! You need permission before you can access this valuable stuff.”

Must Read

So, What Exactly is CoreLogic?

First off, who is CoreLogic? Imagine a giant, super-organized filing cabinet for a huge chunk of information about homeowners and property. CoreLogic is one of those companies that collects and manages a lot of data related to mortgages, property values, and the like. They’re a big player in the world of real estate data. Because they have this information, they are also a place where someone trying to impersonate you might try to access your data.

Now, "Opt Out" and "Security Freeze" are the key phrases here. "Opt Out" means you’re actively choosing not to have your information used in certain ways, and "Security Freeze" is the action that puts a big “do not disturb” sign on your credit file. It’s like telling the credit bureaus (the main companies that track your credit history) and other data providers like CoreLogic: “Unless I say so, nobody gets to see my credit report for new applications.”

Why Should You Even Care About This?

Let’s say you’re planning a surprise birthday party for your best friend. You’ve got the decorations, the cake, and you’ve been secretly inviting guests. Imagine if suddenly, a bunch of strangers showed up, uninvited, trying to join the party and eat all the cake! That’s kind of what identity theft can feel like. It’s your life, your identity, and suddenly some unauthorized people are trying to party with it. A security freeze is like sending out those secret invitations and having a bouncer at the door who checks everyone’s invitation before they come in.

Think about it: have you ever applied for a new credit card, a car loan, or even a new phone plan? They’re going to ask to check your credit. If you have a security freeze in place, that application process will be temporarily paused until you temporarily “unfreeze” your credit. This is a good thing because it means a scammer, who doesn’t have your permission or your personal details, can’t just waltz in and open up a bunch of accounts in your name.

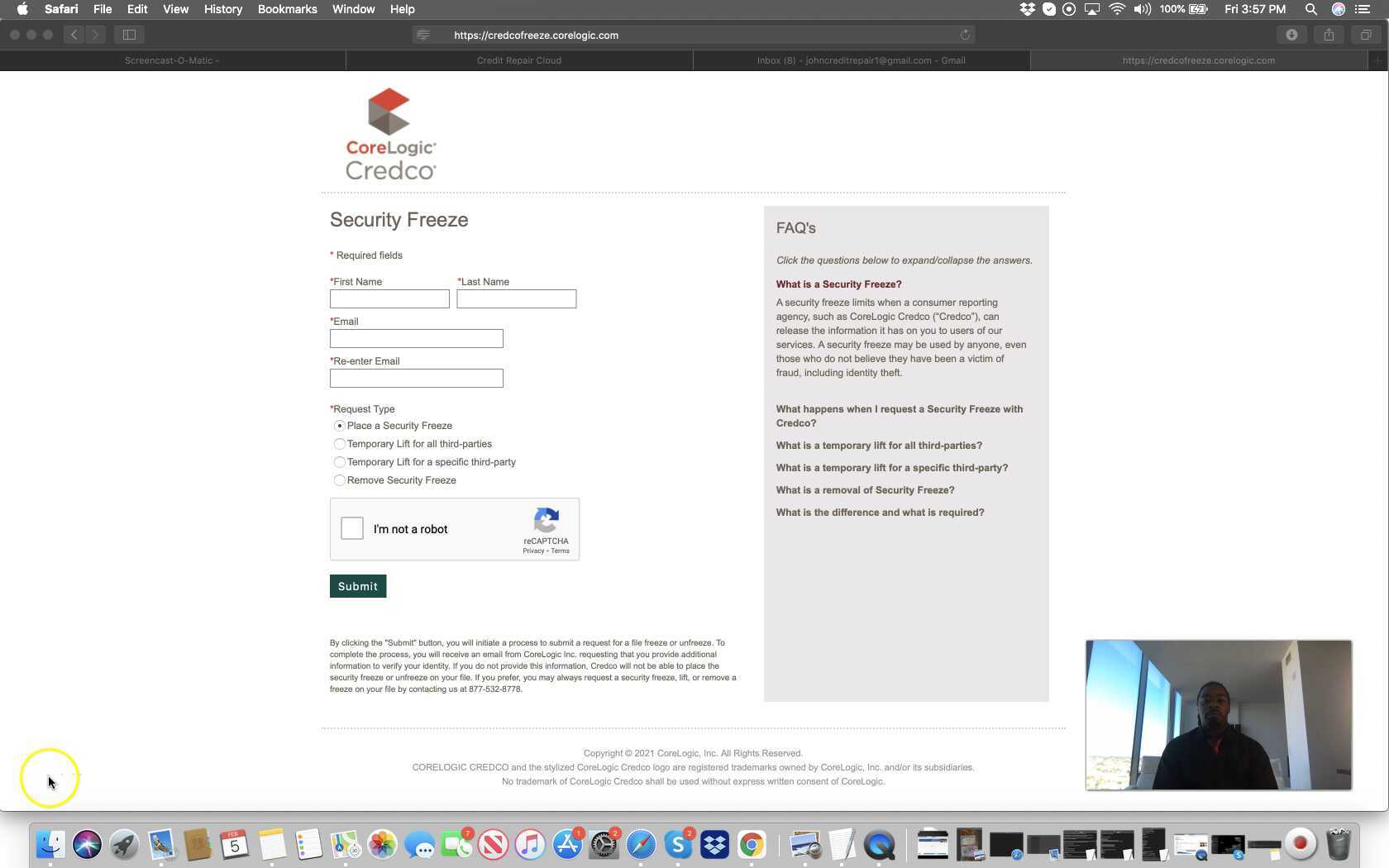

Making it Happen: The "Opt Out" Part

The "opt out" part is where you proactively tell these companies, "Hey, I want a higher level of protection for my personal information." When it comes to credit bureaus, this is a well-established process. But CoreLogic, and similar data aggregators, also have ways you can opt out of certain data sharing or request a freeze.

The easiest way to think about the "opt out" process for places like CoreLogic is to visit their website. They usually have a dedicated section for privacy or security. You’ll likely find information there about how to request a freeze or opt out. It might involve filling out a form, providing some verification details to prove you are indeed you, and then sending it in. It’s like sending in your RSVP for that surprise party – you’re letting them know you want in on the protection!

Sometimes, this involves something called a “security freeze” or a “fraud alert.” A fraud alert is like a warning flag that says, “Be extra careful with this person’s information.” A security freeze is more like a locked door that requires a key (your permission) to open.

The "Security Freeze" – Your Personal Velvet Rope

So, how does the actual “freeze” work? When you place a security freeze with the three major credit bureaus (Equifax, Experian, and TransUnion), it prevents anyone from accessing your credit report without your explicit permission. This is crucial because applying for credit is a primary way identity thieves can monetize your stolen information.

For places like CoreLogic, the concept is similar. They’re not a credit bureau in the same sense, but they do hold sensitive data. Requesting an opt-out or a freeze with them is about limiting who can access or use that data. It’s like putting a special lock on your mailbox that only you have the key for, so nobody can snoop through your mail.

What Happens When You Need to Use Your Credit?

Now, you might be thinking, “But what if I want to buy a house or a car? Won't this freeze cause problems?” Great question! This is where the temporary "thaw" or "unfreeze" comes in. When you need to apply for credit or something similar that requires a credit check, you’ll need to temporarily lift the freeze. You can usually do this by contacting the credit bureaus or the data provider directly, often online, by phone, or by mail.

![CoreLogic Opt Out & Data Removal Guide [2026] | Incogni](https://blog.incogni.com/wp-content/uploads/2023/01/Image-1.png)

Think of it like this: you're going out for a special dinner. You wouldn't wear your pajamas, right? You'd get dressed up. Unfreezing your credit is like putting on your best outfit for that important occasion. Once the application process is complete, you can then re-freeze your credit. It’s a little bit of back-and-forth, but it’s a small price to pay for peace of mind. Many of these services even allow you to set specific dates for unfreezing, so you don't have to remember to refreeze it yourself.

Why It's Worth the Tiny Effort

In our digital age, our personal information is constantly being shared and stored. While much of this is for convenience, it also opens up more avenues for bad actors. Taking the step to opt out and freeze your credit with major bureaus and data aggregators like CoreLogic is like installing a really good security system for your home. You might not need it every single day, but when you do, it's a lifesaver.

It’s about being proactive, about taking control of your digital footprint. It’s about protecting yourself and your loved ones from the headache, the stress, and the financial mess that identity theft can create. So, if you’ve got a few minutes, and you’re feeling like you want to add an extra layer of security to your life, consider looking into the CoreLogic Opt Out Security Freeze and similar measures for your credit reports. It’s a simple step that can make a world of difference in keeping your information safe and sound. Go ahead, give your personal data the VIP treatment it deserves!

![CoreLogic Opt Out & Data Removal Guide [2024] | Incogni](https://blog.incogni.com/wp-content/uploads/2023/01/image-5.png?x67123)