Can I Get A Mortgage At 50

So, you're cruising through life, hitting that fabulous 50 mark, and maybe, just maybe, the dream of homeownership or upgrading to a bigger place is still very much alive. You might be thinking, "Can I even get a mortgage at 50? Isn't that, like, a bit late to the party?" Well, settle in, grab a cuppa, and let's have a chill chat about it. Because the answer, my friends, is a resounding yes, you absolutely can!

It’s a question that pops up more often than you might think. Fifty isn't some magical cutoff date for financial endeavors. Think of it like this: if you can bake a killer sourdough or master a new yoga pose at 50, then navigating the mortgage world is totally within reach.

Age is Just a Number (Mostly!)

Lenders, bless their analytical hearts, are primarily interested in one thing: your ability to repay the loan. Your age is a factor, sure, but it's far from the only, or even the most important, one. They're looking at your financial health, not your birth certificate.

Must Read

Think of it like a dating profile. While age might be a detail, a great job, a stable history, and a good personality (in this case, a good credit score and income!) are what really seal the deal. A 50-year-old with a solid income and a good credit history is often a much more attractive prospect than a younger person with shaky finances.

What Lenders Really Care About

So, what exactly are these lenders scrutinizing? Let's break it down:

Your Income: The Bedrock of Repayment

This is probably the biggest piece of the puzzle. Lenders want to see a consistent and reliable income. This could be from your current job, a business you own, or even rental properties. The more stable your income, the more confident they are that you can handle those monthly mortgage payments.

If you're still working, and have years ahead of you before retirement, that's a huge plus. Even if retirement is on the horizon, lenders will look at your projected income and savings to ensure you can manage the loan comfortably. It’s like planning a long road trip; you need to know you’ve got enough fuel (income) to get to your destination.

Credit Score: Your Financial Report Card

Your credit score is like your financial report card. A good score shows lenders that you're responsible with money. It means you've paid bills on time, managed debt wisely, and generally have a track record of financial reliability. A higher credit score can also mean better interest rates, which is always a win!

If your credit score isn't quite where you'd like it to be, don't despair! There are plenty of resources and strategies to improve it. Think of it as giving your financial report card a little pre-exam cram session. It might take a little effort, but the payoff is significant.

Debt-to-Income Ratio: Keeping Things in Balance

This is a fancy way of saying how much of your monthly income goes towards paying off debts. Lenders want to see that you're not already stretched too thin. If you have a lot of existing debt (car loans, credit cards, student loans), it can impact your ability to take on a new mortgage.

A lower debt-to-income ratio is generally better. It shows you have more disposable income to cover your mortgage payments. So, if you’re thinking about a mortgage, it might be a good time to look at ways to reduce some of those existing debts.

Savings and Down Payment: Showing Your Commitment

Having a decent amount of savings is crucial. This shows lenders that you have a financial cushion and are serious about the purchase. A larger down payment can also reduce the amount you need to borrow, which can lead to a smaller mortgage and potentially lower monthly payments.

Think of your down payment as your way of saying, "I'm in this to win it!" It demonstrates your commitment and can make lenders feel more secure about offering you the loan. Plus, a bigger down payment means less interest paid over the life of the loan – a sweet bonus!

The "Retirement Question"

Okay, so what about when retirement is closer or has already arrived? This is where things get a little more nuanced, but still very doable.

Income in Retirement

If you're retired, lenders will look at your retirement income sources. This could be from pensions, social security, investments, or annuities. The key is proving that this income will be stable and sufficient for the duration of the mortgage term.

It's like having a reliable stream of income from a favorite hobby that you've turned into a business. As long as that stream is steady, lenders are happy. Sometimes, using funds from retirement accounts as a down payment is also an option, but it's always wise to consult with a financial advisor on this.

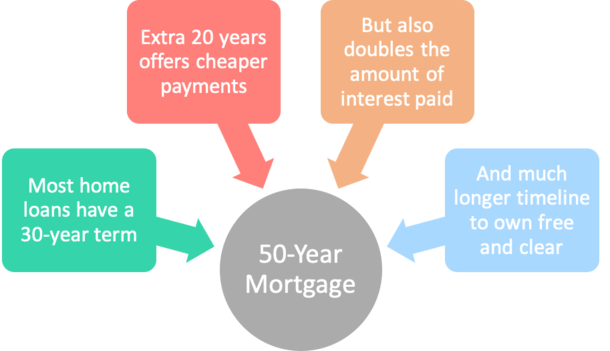

Mortgage Term Length

This is where age can play a slightly bigger role, but not in a way that automatically disqualifies you. Lenders have limits on how long they'll offer mortgages. Typically, the mortgage term should end before or shortly after you reach a certain age, often around 70 or 75.

So, if you're 50 and want a 30-year mortgage, that might be pushing it a bit for some lenders. But a 15-year or even a 20-year mortgage? Absolutely achievable! It just means your monthly payments might be a bit higher, but you'll also pay off the loan faster. It's like choosing between a leisurely stroll and a brisk walk; both get you there, just at a different pace.

Why Getting a Mortgage at 50 is Actually Cool

Let's flip the script. Instead of seeing your age as a hurdle, let's see the advantages:

Wisdom and Stability

At 50, you've likely accumulated a wealth of life experience, including financial experience. You're probably more stable in your career and less likely to make impulsive financial decisions than someone much younger. This maturity is a big plus for lenders.

Established Financial History

You’ve had more time to build a solid financial history. This means more opportunities to establish a good credit score, save money, and demonstrate responsible financial behavior. It’s like having a longer resume with more impressive accomplishments!

Potential for Larger Down Payments

With years of saving and investing, you might have a more substantial down payment ready. This can open doors to better loan terms and a more favorable mortgage. It’s like showing up to a potluck with a gourmet dish instead of just a bag of chips!

Tips for Success

Ready to make that dream a reality? Here are some chill tips:

Get Your Financial House in Order

Before you even start talking to lenders, take stock of your finances. Check your credit report, review your income and expenses, and get a clear picture of your financial standing.

Shop Around!

Don't just go with the first lender you find. Compare rates, terms, and fees from different banks, credit unions, and mortgage brokers. A little comparison shopping can save you a lot of money in the long run.

Consider a Mortgage Broker

A good mortgage broker can be your best friend. They work with multiple lenders and can help you find the best mortgage product for your situation. They're like your personal mortgage matchmaker!

Be Prepared to Explain Your Situation

Lenders might want to understand your income sources, especially if you're nearing retirement. Be ready to provide clear and organized documentation.

So, to wrap it all up, can you get a mortgage at 50? The answer is a confident yes! It’s not about your age; it’s about your financial readiness. Embrace your experience, get your ducks in a row, and you might just be unlocking the door to your next chapter sooner than you think. Happy house hunting!