Can I Buy A House For My Child

Ah, the age-old question that pops up when you're sipping your morning coffee, scrolling through Zillow, or maybe even after a particularly successful bake sale. "Can I buy a house for my child?" It’s a thought that can feel as grand as winning the lottery, and sometimes, just as far-fetched. But let's be honest, who hasn't fantasized about handing over the keys to their little one, watching their face light up like it’s Christmas morning and their birthday all rolled into one?

It’s a dream born out of love, pure and simple. We want our kids to have a safe, cozy nest, a place to call their own, a launching pad for their future. It’s like wanting them to have the best superhero cape, the coolest bike, or the most sprinkles on their ice cream. Except, you know, a bit more... bricks and mortar.

Think about it. We spend years nurturing them, teaching them to tie their shoes, to ride a bike without wobbly knees, and how to, ahem, mostly clean their room. And then, BAM! They're grown. Suddenly, they're off, facing the world, and we're left wondering if they're eating enough vegetables and if their landlord really fixes that leaky faucet. Buying them a house feels like the ultimate parental mic-drop, a "job well done" statement in concrete and drywall.

Must Read

But, let's pump the brakes a little, shall we? This isn't quite as straightforward as picking out a new throw pillow for the living room. It involves a whole lot more than just a quick trip to IKEA. We’re talking about things like money. Big, significant, often scary money. The kind of money that makes you re-evaluate your Netflix subscription or contemplate selling that slightly-too-small designer handbag you've been clinging to for sentimental reasons.

So, can you actually buy a house for your child? The short answer is: maybe. It's less about a definitive "yes" or "no" and more about a hearty "it depends." It depends on a whole constellation of factors, like a complicated recipe where one missing ingredient can change the whole flavour profile.

The Big Kahuna: Your Financial Landscape

First and foremost, we need to talk about the elephant in the room. Or rather, the mansion in the room: your own financial health. Are you sitting pretty with a Scrooge McDuck-esque vault of gold coins? Or are you more like a squirrel, carefully hoarding nuts for the winter (and maybe a few unexpected avocado toast splurges)?

Buying a house for someone else, even your own flesh and blood, is a major financial commitment. It’s not like buying them a fancy new gaming console that they’ll probably get bored of in three months. This is a commitment that can stretch for decades. So, before you start drafting blueprints and picking out paint swatches in your head, take a good, hard look at your own finances.

Are your retirement plans on solid ground? Do you have a comfortable emergency fund, the kind that makes you feel like you could weather a zombie apocalypse (or at least a sudden job loss)? If the answer to these questions is a resounding "uh oh," then perhaps it's time to put the house-buying dream on the back burner and focus on shoring up your own nest egg. It’s like trying to build a sturdy birdhouse for your chick while your own perch is looking a bit rickety.

Think of it this way: you wouldn't lend your car to a new driver without making sure they know the difference between the gas and brake pedals, right? It’s the same principle with a house. You need to be in a stable financial position yourself before you can responsibly take on this kind of responsibility for someone else.

The "How Much" Question: A Numbers Game

Okay, so you’ve done your financial deep dive, and you’re feeling reasonably confident. Now comes the really fun part: the numbers. How much house are we even talking about? Is it a charming starter cottage, a sprawling family estate, or somewhere in between? This is where the real estate market starts to do its funky dance.

Prices vary wildly, as anyone who’s ever browsed Zillow at 2 AM knows. You could be looking at a cozy fixer-upper in a quiet suburb, or a shoebox apartment in a bustling city that costs more than a small island. Your child’s location preferences, their dreams (and yours!), and the current market conditions will all play a massive role.

Then there are the other costs. It’s not just the sticker price. We’re talking about down payments, closing costs, property taxes, insurance, potential renovations, and the inevitable, "oh, the dishwasher sounds funny" moments. It's like planning a wedding; the dress is just the beginning!

Down Payment: This is usually the biggest hurdle. It's the initial chunk of cash you hand over to make the purchase official. The more you can put down, the less you'll need to borrow, and the lower your monthly mortgage payments will be. It's the financial equivalent of a really good head start.

Closing Costs: These are a collection of fees that come with finalizing a mortgage. Think of them as the administrative sprinkles on your house-buying cupcake. They can include things like appraisal fees, title insurance, and attorney fees. They’re not always a huge percentage, but they can add up faster than you think.

Ongoing Costs: This is the gift that keeps on giving. Property taxes, homeowner's insurance, utilities, and regular maintenance. These are the expenses your child will be responsible for, but you need to factor them into your initial planning. Imagine buying them a high-maintenance poodle; you need to be prepared for the grooming bills!

If the thought of all these numbers makes your eyes water, you're not alone. It’s enough to make anyone want to retreat to the comfort of their current, perfectly adequate rental situation.

Paths to Parenthood Property Ownership: Options Galore!

So, let's say you've crunched the numbers, done the financial gymnastics, and you're ready to explore how you might actually make this happen. It's not just a matter of handing over a giant check (though that would be lovely!). There are several ways you can go about it.

1. The Direct Purchase: A Straightforward (and Spendy) Route

This is the most obvious method. You literally buy the house, and then you decide what happens next. You could gift it to them outright, or you could set up a payment plan. This is the most common scenario people imagine, and it’s also, typically, the most financially demanding.

If you have the cash lying around, or you're willing to tap into equity from your own home (more on that later!), this is a direct and relatively simple approach. Think of it as buying them a brand new, top-of-the-line skateboard. It’s all yours, ready to go.

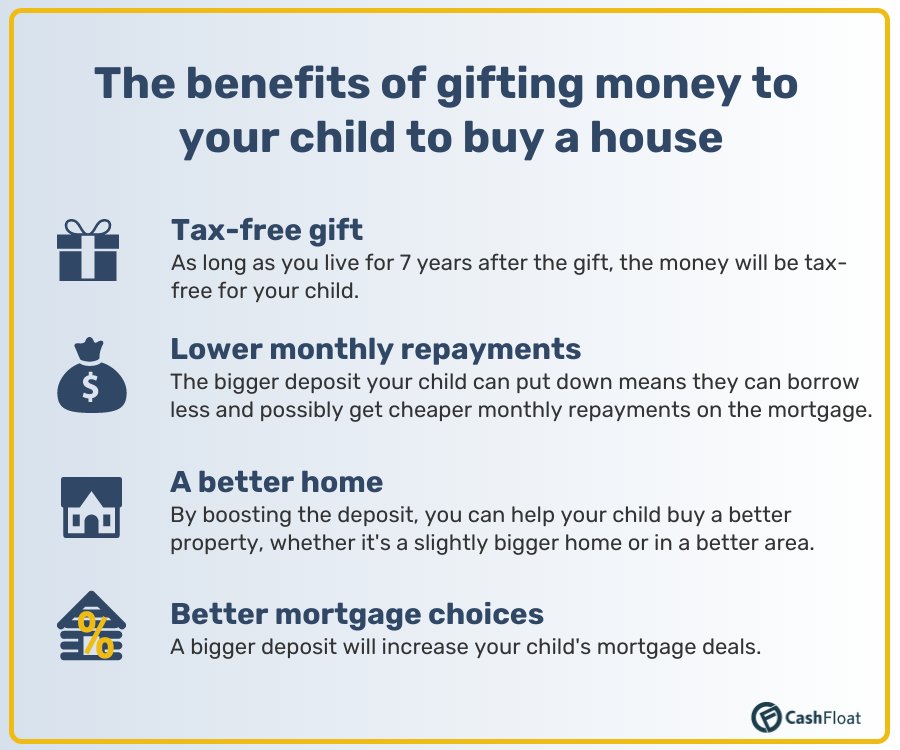

However, there are tax implications to consider. Gifting a significant amount of money can trigger gift taxes, so it’s always wise to consult with a tax professional. They can help you navigate these waters without capsizing your financial boat.

2. The Co-Signer: A Helping Hand, Not a Full Handout

This is a popular option for parents who want to help their child secure a mortgage but can't or don't want to foot the entire bill. As a co-signer, you're essentially putting your own credit on the line to help your child qualify for a loan. It's like being the guarantor for their first car loan, but on a much grander scale.

This means that if your child defaults on their mortgage payments, you are on the hook. This is a serious responsibility and one that should not be taken lightly. You need to have a very open and honest conversation with your child about their financial responsibilities and their ability to manage the mortgage payments independently.

It can be a win-win. Your child gets a home, and you help them build their credit and equity. But remember, their financial mishaps can become your financial headaches. It's like offering to spot your friend at the casino; you're hoping for the best, but you’re also prepared for the worst!

3. The Down Payment Gift: A Generous Boost

Instead of buying the whole house, you could simply provide a significant portion of the down payment. This makes it much easier for your child to qualify for a mortgage on their own and significantly reduces their monthly payments. It’s like giving them a really powerful cheat code for the home-buying game.

This is a fantastic way to help without taking on the full burden of the mortgage. Your child still owns the house and is responsible for the payments, but your contribution gives them a much stronger footing. This is often considered a more manageable option for parents who want to help but have other financial priorities.

Again, be aware of gift tax rules. Depending on the amount, you might need to file a gift tax return.

4. Loaning the Money: A Formal Arrangement

You could loan your child the money for a down payment or even the entire purchase price. This would typically be structured with a formal loan agreement, including interest rates and repayment terms. It's essentially you acting as the bank.

This offers more control than a gift, as you have a clear understanding of when and how you'll be repaid. It's like lending your child your prized toolkit; you expect it back in good condition, and you'll have terms about its use.

Make sure the loan agreement is clear and fair. This can prevent misunderstandings down the road. It's also important to consider how this loan might affect your own financial planning and liquidity.

5. Joint Ownership: A Shared Stake

You could jointly purchase the house with your child. This means you'd both be on the mortgage and the title. It's like buying a boat together; you share the ownership and the responsibilities.

This can be a good option if your child’s credit isn’t quite strong enough on its own, or if you want to ensure you have a say in the property. However, it means you'll be financially linked to the property and its upkeep for as long as you're a co-owner.

When the time is right, you can then discuss how to transfer your share to your child, whether through a buyout or a gift. This requires careful planning and legal advice to ensure a smooth transition.

The "Why": More Than Just Bricks and Mortar

Beyond the financial nuts and bolts, there’s the emotional aspect. Why do we even want to do this? It's not just about giving our kids a place to live. It's about giving them a sense of stability, a foundation upon which they can build their lives. It’s about saying, "I believe in you, and I'm here to support your dreams."

It’s about seeing them plant roots, create memories, and experience the joys and challenges of homeownership. It’s about watching them paint a room their favourite colour, even if it’s a shade of neon green that makes your eyes water. It’s about them hosting their own dinner parties, their own holiday gatherings, their own little slice of life.

It can be a legacy, a tangible expression of your love and commitment. It’s a way of saying, "I’ve always been there for you, and I want you to have this security." It's a monumental gift, a true act of love.

The "What Ifs": Considerations and Cautions

Now, let's talk about the important stuff. Before you go signing on dotted lines and emptying your savings account, there are some crucial things to consider. It's like checking the weather before a big picnic; you want to be prepared for anything.

The Relationship Factor: Keep it Healthy!

This is perhaps the most delicate aspect. Mixing finances with family can be a recipe for disaster if not handled with extreme care. Money can change relationships, and even the most loving parent-child dynamic can be strained by financial entanglements.

Have brutally honest conversations with your child. What are their expectations? What are their responsibilities? What happens if they can't make payments? What happens if you can't afford to help anymore?

It’s essential to set clear boundaries and expectations from the outset. If you’re gifting the house, make it clear. If you’re co-signing, make clear the responsibilities. If you’re expecting repayment, ensure it’s documented. This isn't about being mistrustful; it's about being prepared and preserving your relationship.

Imagine you’re lending your child your favourite sweater. You want them to love it and take care of it, but you also want it back in the same condition. A clear understanding upfront prevents awkward conversations later.

Tax Implications: The Unavoidable Truth

As mentioned before, gifting significant amounts of money can have tax consequences. You might be subject to federal and state gift taxes. It’s crucial to consult with a tax advisor to understand these implications and plan accordingly. They can help you structure the transaction in the most tax-efficient way possible.

This is not the time to wing it. Tax laws are complex, and making a mistake can be costly. Think of them as the grumpy but necessary referees of the financial world.

Legal Advice: Your Safety Net

Buying a house is a legal transaction. When you’re adding another person into the mix, or even gifting a property, it’s wise to get legal advice. A real estate attorney can help you draft any necessary agreements, ensure proper titling, and protect both your interests and your child’s.

This is your legal safety net. It’s better to have it and not need it than to need it and not have it. They're like the wise elders of the legal kingdom, guiding you through the labyrinth of property law.

The Bottom Line: Is it a Good Idea?

So, after all this, can you buy a house for your child? Yes, you absolutely can, provided you’ve done your homework, assessed your financial situation honestly, and are prepared for the responsibilities involved. It’s a beautiful gesture of love and support, a way to give your child a significant head start in life.

But it’s not a decision to be taken lightly. It requires careful planning, open communication, and a realistic understanding of the financial and emotional commitment. It’s like deciding to adopt a puppy; it’s incredibly rewarding, but it’s a commitment that will impact your life for years to come.

Ultimately, the best way to answer this question is to sit down, have those honest conversations with your child, crunch the numbers with a clear head, and consult with professionals. If it aligns with your financial capabilities and your child's needs, it can be one of the most meaningful and impactful gifts you ever give. And who knows, you might even get to crash on their sofa when they’re away and you need a change of scenery!