Is 657 A Bad Credit Score India

So, I was chatting with my friend Priya the other day. She’s been eyeing this gorgeous little apartment downtown, the one with the balcony that overlooks that amazing park. You know the one? She’s all excited, picturing herself sipping her chai there every morning. But then, the landlord, bless his heart, asks for a credit score. Priya, who’s usually as cool as a cucumber, starts sweating bullets. She pulls out her phone, fiddles around for a bit, and then her face falls. "Oh no," she whispers, "it's 657."

I immediately thought, "657? Is that like… a failing grade in adulting?" Because, let's be honest, when it comes to credit scores, we’re bombarded with numbers. We see those fancy infographics that show you the "good," the "great," and the "OMG, run away!" zones. And somewhere in the murky middle, there’s this number: 657. So, the burning question, for Priya and probably for a lot of you reading this, is: Is 657 a bad credit score in India? Let’s dive in, shall we?

The Great Indian Credit Score Mystery

First off, let’s get one thing straight: there isn't a single, universally agreed-upon "bad" number for credit scores in India. Unlike some countries where a specific cutoff is pretty well-known, India's credit ecosystem is still evolving. Think of it less like a strict school grading system and more like a slightly chaotic but generally useful report card.

Must Read

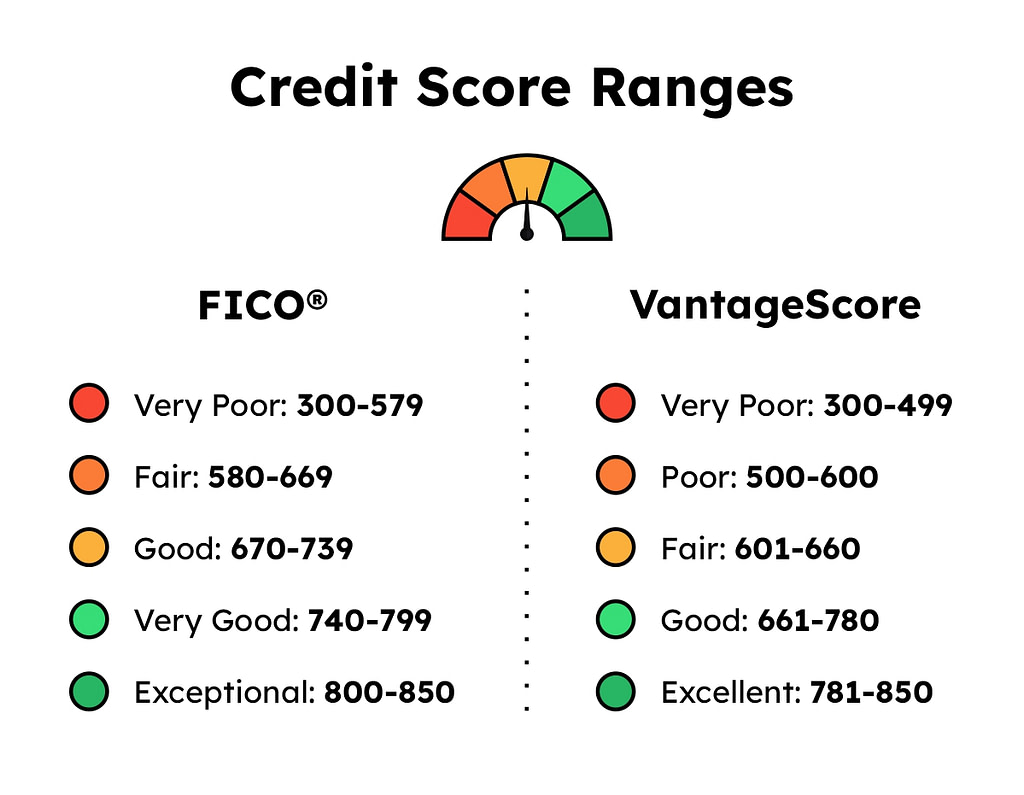

You've got your Credit Information Bureau (India) Limited (CIBIL) score, which is probably the most talked about. Then there's Experian, Equifax, and CRIF High Mark. They all do their thing, collecting your financial history and spitting out a score. And the interesting thing? These scores can vary slightly between agencies. Weird, right? It's like having three different teachers grade the same exam and getting three different marks. What are you gonna do?

So, Where Does 657 Fit In?

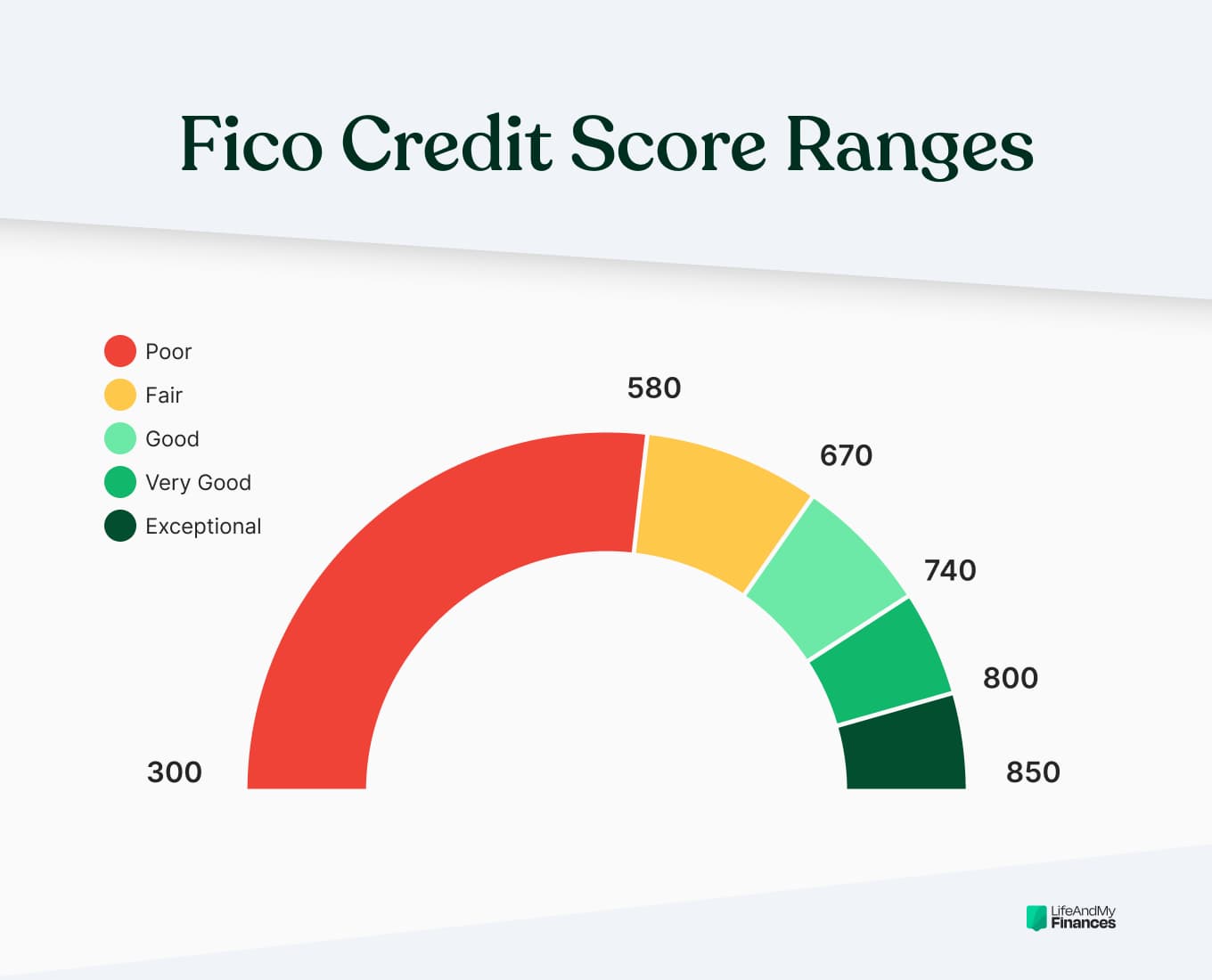

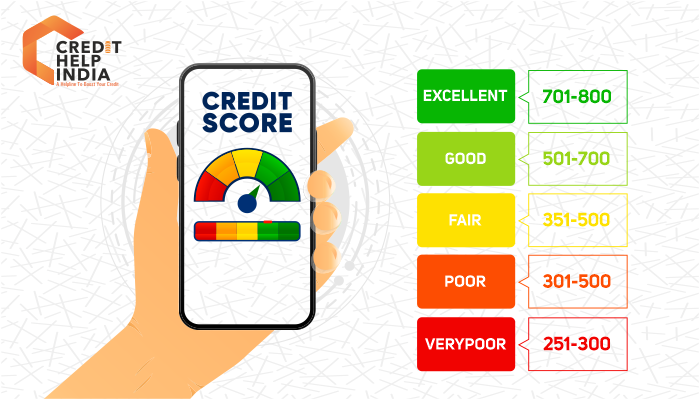

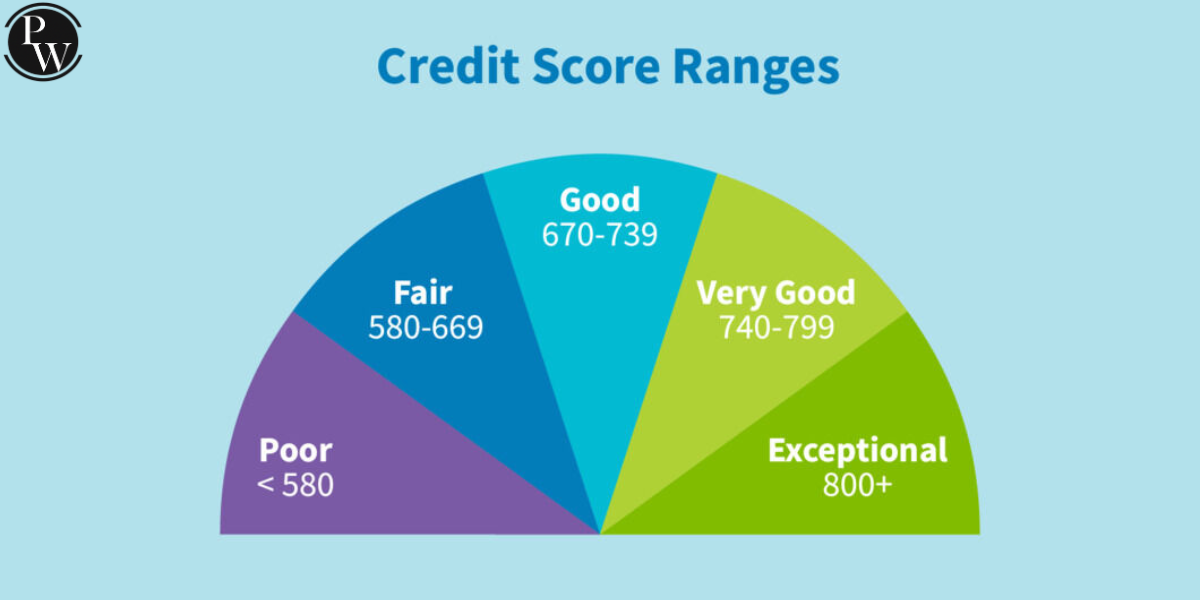

Generally speaking, most lenders in India look at a score range from 300 to 900. Now, 900 is the superhero of credit scores, the stuff of dreams and instant loan approvals. The lower you go, the more… interesting your financial story becomes, from a lender's perspective.

A score like 657 typically falls into what’s often called the "fair" or "average" category. It’s not the "excellent" or "good" tier where you’ll get the red carpet treatment from banks. But it’s also not the "very poor" or "risky" zone where doors slam shut with a resounding thud.

Let's put it this way: if "excellent" is a Michelin-star restaurant and "very poor" is a roadside dhaba with questionable hygiene, then 657 is probably that cozy neighbourhood cafe. You can still get a decent meal, but don't expect them to whip up a seven-course tasting menu on demand.

What Does 657 Actually Mean for You?

Okay, so 657 isn't a screaming siren of financial doom, but it's also not a free pass. Here's the lowdown on what a score in this range might mean:

- Loan Approvals: You'll likely still be able to get loans – personal loans, home loans, car loans. However, don't be surprised if the interest rates are a tad higher than someone with a stellar score. Lenders see a 657 as a bit more of a gamble, so they charge a premium to offset that perceived risk. Think of it as paying a little extra for peace of mind, but for them!

- Loan Amounts: The amount you can borrow might also be capped. Lenders might be hesitant to approve very large sums for individuals with average credit scores. They prefer to lend smaller amounts that are easier to manage.

- Credit Card Offers: You'll probably get offers for credit cards, but they might be the more basic ones with lower credit limits and fewer fancy rewards. Those premium travel cards with airport lounge access? They’re probably out of reach for now.

- Rental Agreements: Like Priya’s landlord situation, a 657 might raise a few eyebrows. Some landlords, especially those who are more risk-averse, might see it as a sign of potential instability or a less reliable tenant. You might need to be prepared to offer a larger security deposit or provide a guarantor. Always a fun conversation to have, isn't it?

- Negotiating Power: Your ability to negotiate terms and interest rates will be limited. With a higher score, you have leverage. With a 657, you're more likely to accept the terms offered.

Why Might Your Score Be Stuck Around 657?

This is where the detective work begins. A score of 657 isn't usually a result of one massive financial faux pas. It's more often a pattern of smaller issues, or perhaps a lack of a strong credit history. Let's ponder some common culprits:

- Late Payments: This is the biggie. Even a few late payments on credit cards or loans can significantly drag down your score. It signals to lenders that you're not the most reliable borrower. We’ve all been there, right? That moment you realize your EMIs were due yesterday. Oops.

- High Credit Utilization: This refers to the amount of credit you're using compared to your total available credit. If you have a credit card limit of ₹1 lakh and you're consistently using ₹80,000 of it, your utilization is 80%. High utilization (generally above 30%) can indicate you're overextended.

- Limited Credit History: If you're relatively new to the credit game, or you haven't used credit much, your score might be lower because there’s just not enough data for lenders to assess your risk accurately. It's like trying to judge a book by its cover when the cover is still blank.

- Too Many Recent Credit Applications: Applying for multiple loans or credit cards in a short period can make you look desperate or risky to lenders. Each inquiry leaves a small mark on your credit report.

- Existing Debt: A large amount of outstanding debt, even if paid on time, can negatively impact your score. It shows you have significant financial obligations.

- Errors on Your Credit Report: It's not unheard of for credit reports to have mistakes. Wrong addresses, incorrect loan details, or even accounts you never opened can be on there. This is why regularly checking your report is super important.

The Good News: It's Not Permanent!

The most crucial thing to understand is that a 657 is not a life sentence. It’s a temporary setback. The beauty of credit scores is that they are dynamic and can be improved with consistent good financial habits. So, while Priya might be stressing about that apartment right now, she can absolutely work towards a better score for future endeavors.

Here’s your action plan, should you find yourself in a similar score bracket:

How to Boost Your 657 Score

- Pay Your Bills On Time, Every Time: This is non-negotiable. Set up auto-debits, reminders, whatever it takes. Even one day late can hurt. Seriously, set those alarms!

- Reduce Credit Utilization: Aim to keep your credit card balances below 30% of your limit. If possible, pay down your balances significantly. This is one of the quickest ways to see an improvement.

- Don't Close Old, Unused Credit Cards (Usually): As long as they don't have annual fees you're unwilling to pay, keeping older, unused credit cards open can help your credit utilization ratio by increasing your total available credit.

- Avoid Unnecessary Credit Applications: Be selective when applying for new credit. Only apply when you truly need it and have a good chance of approval.

- Check Your Credit Report Regularly: Get your free credit report from the major agencies (CIBIL, Experian, etc.) at least once a year. Look for errors and dispute them immediately if you find any.

- Consider a Secured Credit Card or Small Loan: If your credit history is very limited, a secured credit card (where you deposit money as collateral) or a small, short-term loan that you repay diligently can help build a positive track record.

- Diversify Your Credit Mix (Over Time): Having a mix of credit types (like credit cards and installment loans) can be beneficial, but don't open new accounts just for the sake of it. This is a long-term strategy.

The Bottom Line: 657 is a Stepping Stone

So, is 657 a bad credit score in India? It’s more of a "needs improvement" score. It’s the score that tells lenders, "I’m trying, but I haven’t quite mastered the art of perfect financial management yet." It means you might face slightly higher interest rates, smaller loan amounts, and potentially some resistance from landlords or service providers.

But here’s the beautiful part: your credit score is a reflection of your financial behavior, and behavior can be changed. Priya, after our chat, decided to focus on paying down her credit card balances and setting up more reminders. She's not giving up on that apartment; she's just going to work on her creditworthiness first.

Think of your 657 score not as a judgment, but as a roadmap. It shows you where you are and highlights the areas you need to work on. With a little discipline, patience, and the right strategies, you can absolutely move that number upwards. Soon enough, you’ll be the one getting those coveted loan offers and landlord approvals, maybe even with a little extra wiggle room to negotiate. Now, go forth and conquer that credit score!